Why This Story Matters

The headlines about Ontario’s housing market in 2025 painted a picture of doom: “Market Dying,” “Historic Lows,” “Prices Plummet.” These emotionally charged narratives dominated social media feeds and water cooler conversations across the Greater Toronto Area. But here’s what the data actually shows: 2025 wasn’t the year the market collapsed—it was the year fundamentals returned.

For first-time buyers aged 25-55 who spent years watching from the sidelines as prices soared beyond reach, 2025 delivered something unexpected: choice, negotiating power, and predictability. The frenzy ended. The panic subsided. And a healthier, more sustainable market emerged.

This isn’t opinion. This is what happened when you look past the headlines and examine the numbers.

What Actually Changed in 2025

Interest Rates: From Volatility to Stability

The story of 2025 begins with the Bank of Canada’s monetary policy journey. After aggressively hiking rates to combat inflation—reaching 5% in 2023—the central bank executed a carefully calibrated easing cycle throughout 2024 and 2025.

The Timeline:

|

Period |

Policy Rate |

Market Impact |

|---|---|---|

|

Early 2024 |

5.00% |

Peak restrictive policy, buyer confidence suppressed |

|

June 2024 |

4.75% |

First rate cut in 4 years, cautious optimism begins |

|

October 2024 |

3.75% |

Accelerated 50 basis point cut signals commitment |

|

December 2024 |

3.25% |

Second consecutive 50 basis point reduction |

|

March 2025 |

2.75% |

Gradual return to neutral territory |

|

October 2025 |

2.25% |

Final cut of the cycle |

|

December 2025 |

2.25% |

Rate held steady, signaling end of cutting cycle |

By December 10, 2025, the Bank of Canada maintained its policy rate at 2.25%—positioned at the lower end of its neutral range. Governor Tiff Macklem characterized the Canadian economy as “resilient,” and crucially, signaled that the current rate was “about right” to keep inflation near the 2% target while supporting economic adjustment. [Bank of Canada, December 2025]

- Key Reset Insight: 2025 didn’t end with falling rates—it ended with predictable rates. This stability matters more for decision-making than continued cuts ever could.

Fixed mortgage rates, which had hovered in the 5-6% range throughout much of 2024, gradually declined into the low-to-mid 4% range by late 2025, with some 5-year fixed rates available below 4%. [nesto.ca, December 2025]

Home Prices: Correction, Not Collapse

The Ontario housing market experienced what economists call a “price correction”—a return to more sustainable valuations after the unprecedented surge of 2020-2022.

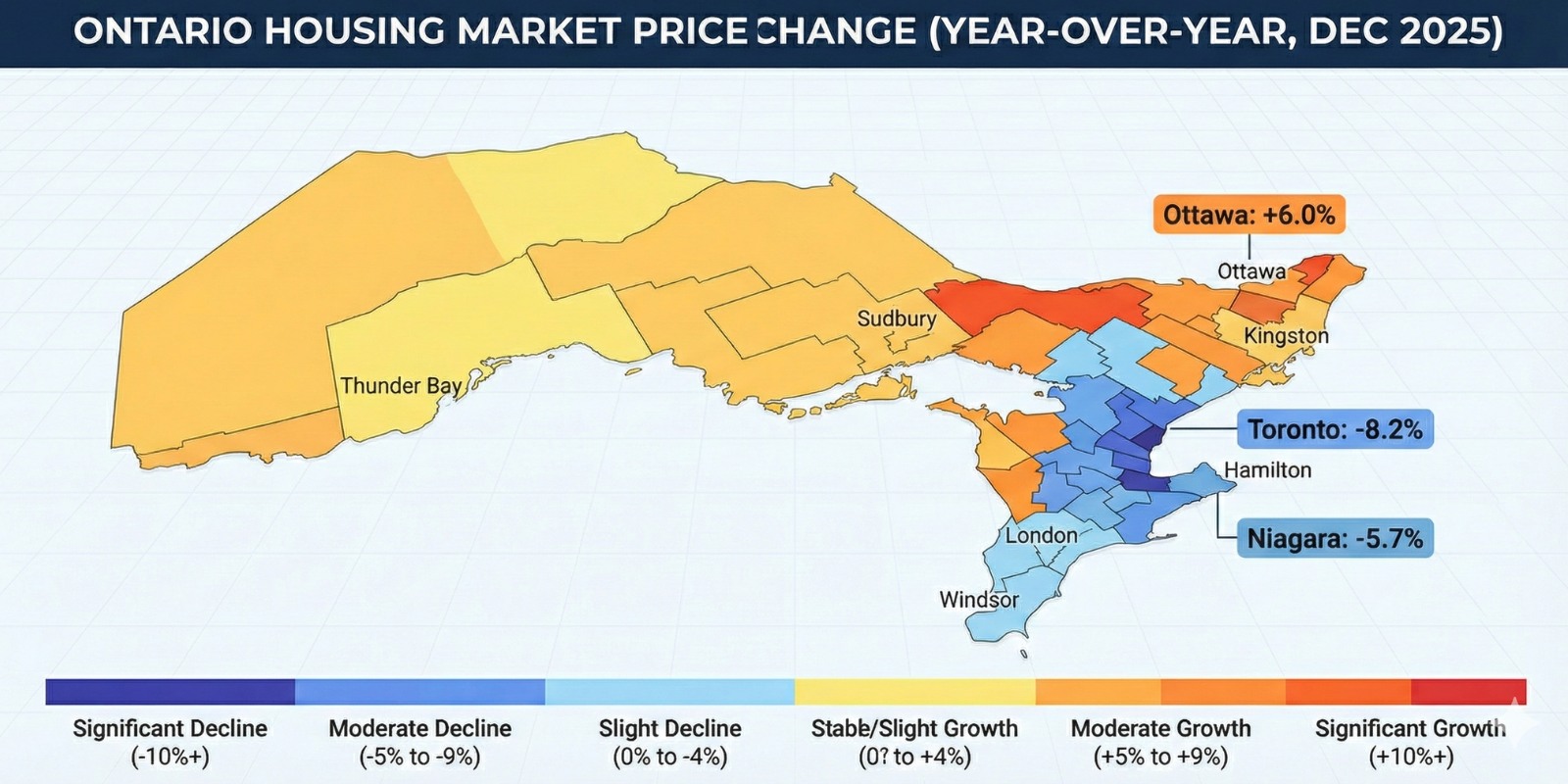

Ontario Price Performance (Year-over-Year, 2025):

|

Region |

Average Price (Nov 2025) |

YoY Change |

Market Condition |

|---|---|---|---|

|

Ontario (Provincial) |

$819,356 |

-5.8% |

Buyer’s Market |

|

GTA Average |

$1,039,458 |

-6.0% |

Buyer’s Market |

|

City of Toronto |

$1,069,807 |

-8.2% |

Buyer’s Market |

|

Mississauga |

$968,036 |

-10.5% |

Buyer’s Market |

|

Brampton |

$934,245 |

-8.4% |

Buyer’s Market |

|

Niagara |

$630,292 |

-5.7% |

Buyer’s Market |

|

Ottawa |

$709,002 |

+6.0% |

Balanced Market |

- Sources: Toronto Regional Real Estate Board, Ontario Real Estate Association, Niagara Association of REALTORS, WOWA.ca, November-December 2025

These numbers tell a nuanced story. Across Ontario, the average home declined approximately 5-7% year-over-year—not the 20-30% crash scenarios many feared. This followed unsustainable growth that saw some markets double in price between 2020-2022.

What Changed Instead of Crashing:

- Overpricing strategies stopped working

- Homes priced correctly still sold within reasonable timeframes

- Buyers regained the ability to negotiate conditions

- Sellers had to align expectations with market reality

In Toronto specifically, the average home price in September 2025 was $960,300, while the GTA composite benchmark price declined to $951,700 by November 2025. [TRREB, nesto.ca, November 2025] Compare this to peak 2022 prices that exceeded $1.3 million in some GTA submarkets, and you see a market that recalibrated rather than imploded.

The Niagara region demonstrated resilience within this broader correction. With an average price of $630,292 in November 2025, Niagara continues to offer more affordable entry points for buyers while experiencing similar market dynamics as the broader Ontario market. The region’s -5.7% year-over-year adjustment aligns it closely with the provincial pattern, indicating healthy market normalization rather than distressed selling. [Niagara Association of REALTORS, November 2025]

- Reset Insight: The market didn’t fall apart. It rebalanced to levels that reflect economic fundamentals rather than speculative fever.

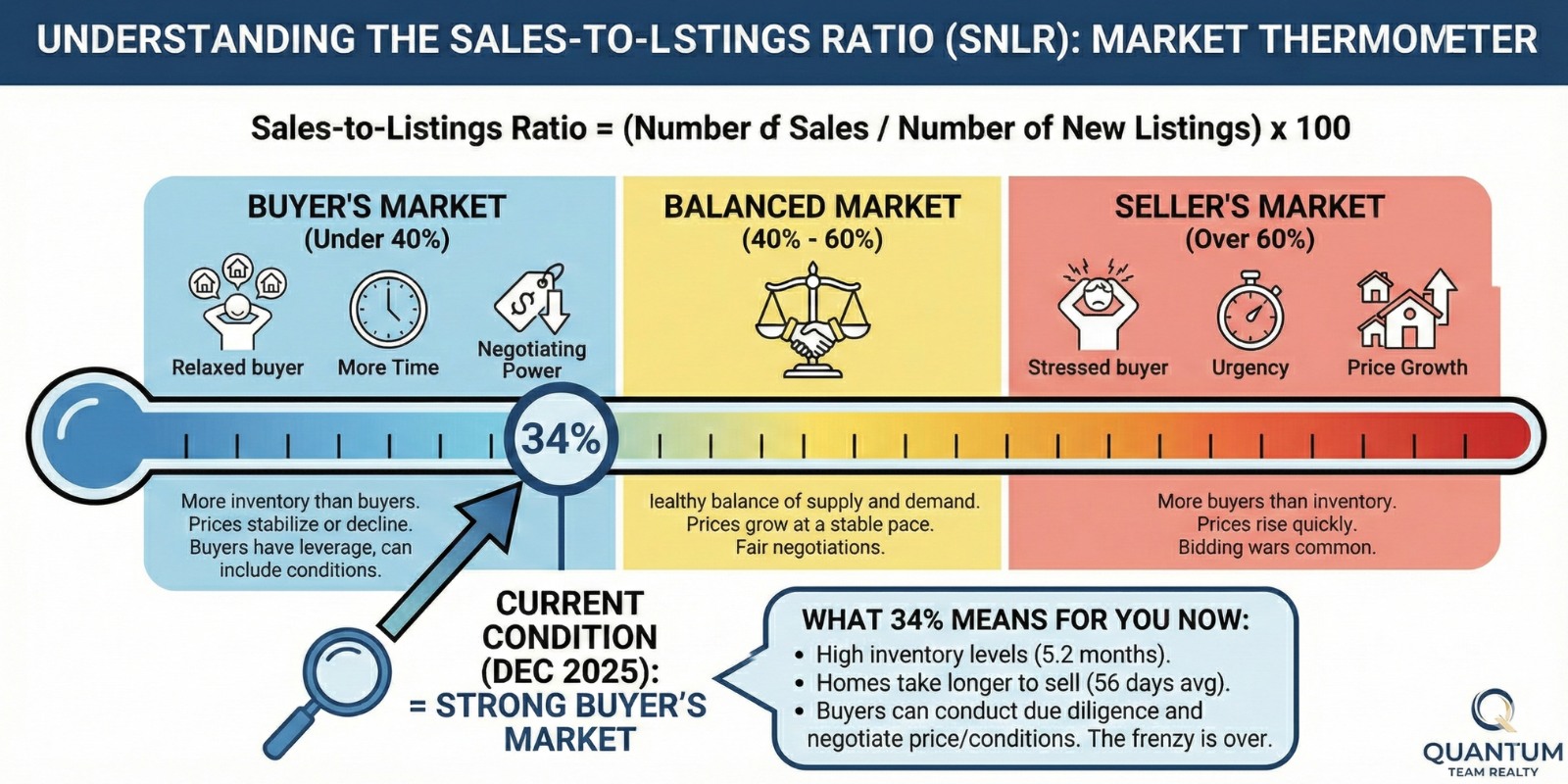

Inventory & Buyer Leverage Returned

Perhaps the most significant shift in 2025 was the transformation from chronic housing shortage to abundant choice.

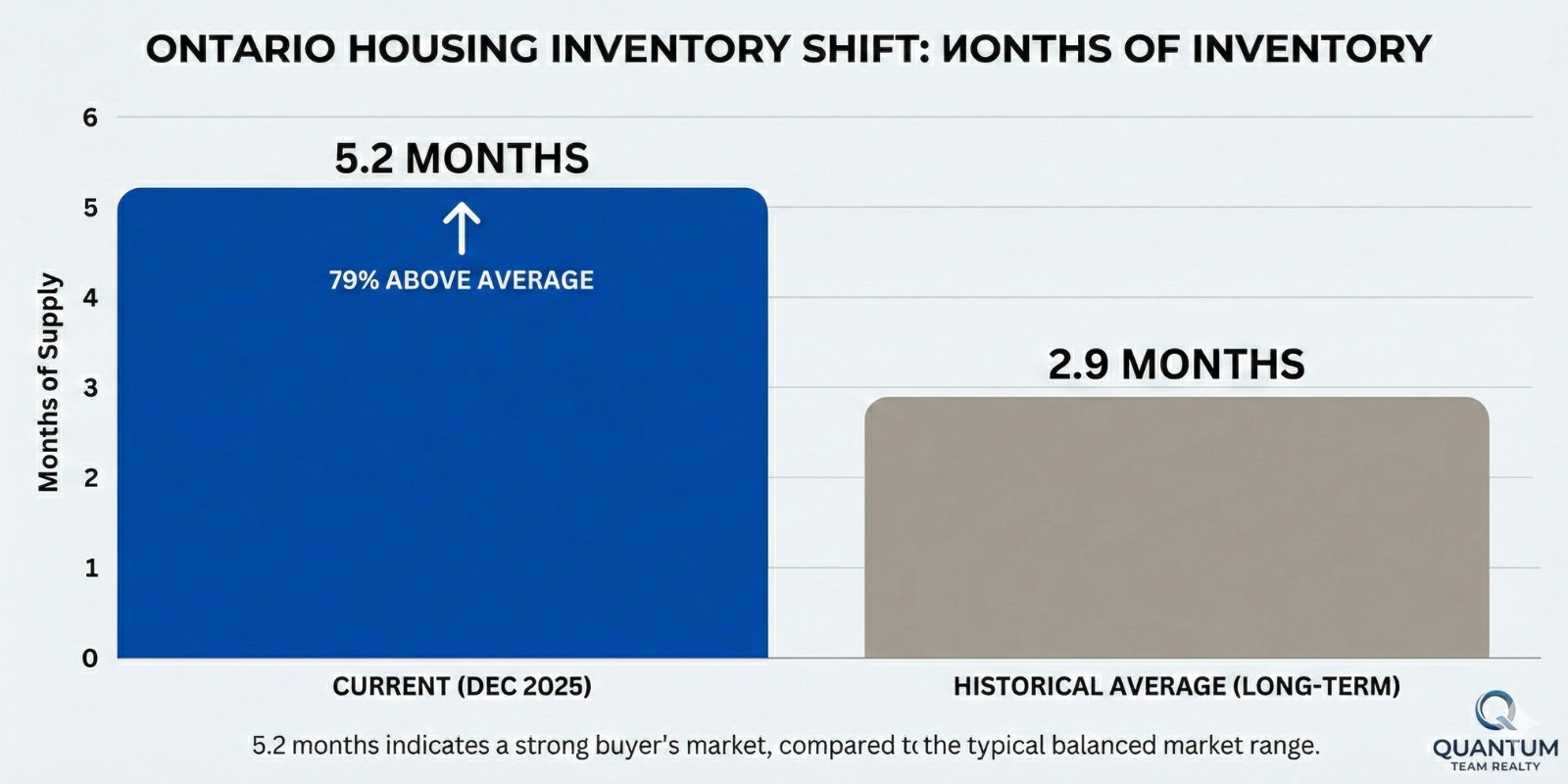

Ontario Inventory Metrics:

|

Region |

Q4 2024 |

Q4 2025 |

Change |

Long-Term Average |

|---|---|---|---|---|

|

Active Listings |

44,000 |

62,868 |

+43% |

40,500 |

|

Months of Inventory |

2.9 |

5.2 |

+79% |

2.9 |

|

Sales-to-New-Listings Ratio |

55% |

34% |

-38% |

48% |

|

Average Days on Market |

25 |

56 |

+124% |

32 |

- Sources: Ontario Real Estate Association, WOWA.ca, Canadian Real Estate Association, November 2025

Active listings in Ontario reached 62,868 units by the end of November 2025—the highest November level in more than 15 years. This represented a 14.3% increase from November 2024 and sat 45.5% above the five-year average. [Ontario Real Estate Association, November 2025]

The months of inventory metric climbed to 5.2 months, nearly double the long-term average of 2.9 months. [Ontario Real Estate Association, November 2025] This means that at the current pace of sales, it would take 5.2 months to sell all available inventory—a stark contrast to the sub-2-month levels that characterized the frenzied 2021-2022 market.

What This Meant for Buyers:

- Choice: Multiple options within their budget and preferred neighborhoods

- Time: Ability to conduct thorough inspections and due diligence

- Negotiation Power: Leverage to negotiate on price, conditions, and closing dates

For the first time since 2019, buyers could pause, compare options, and make calculated decisions rather than submitting blind offers with waived conditions.

- Reset Insight: 2025 returned agency to buyers without triggering a fire sale among sellers.

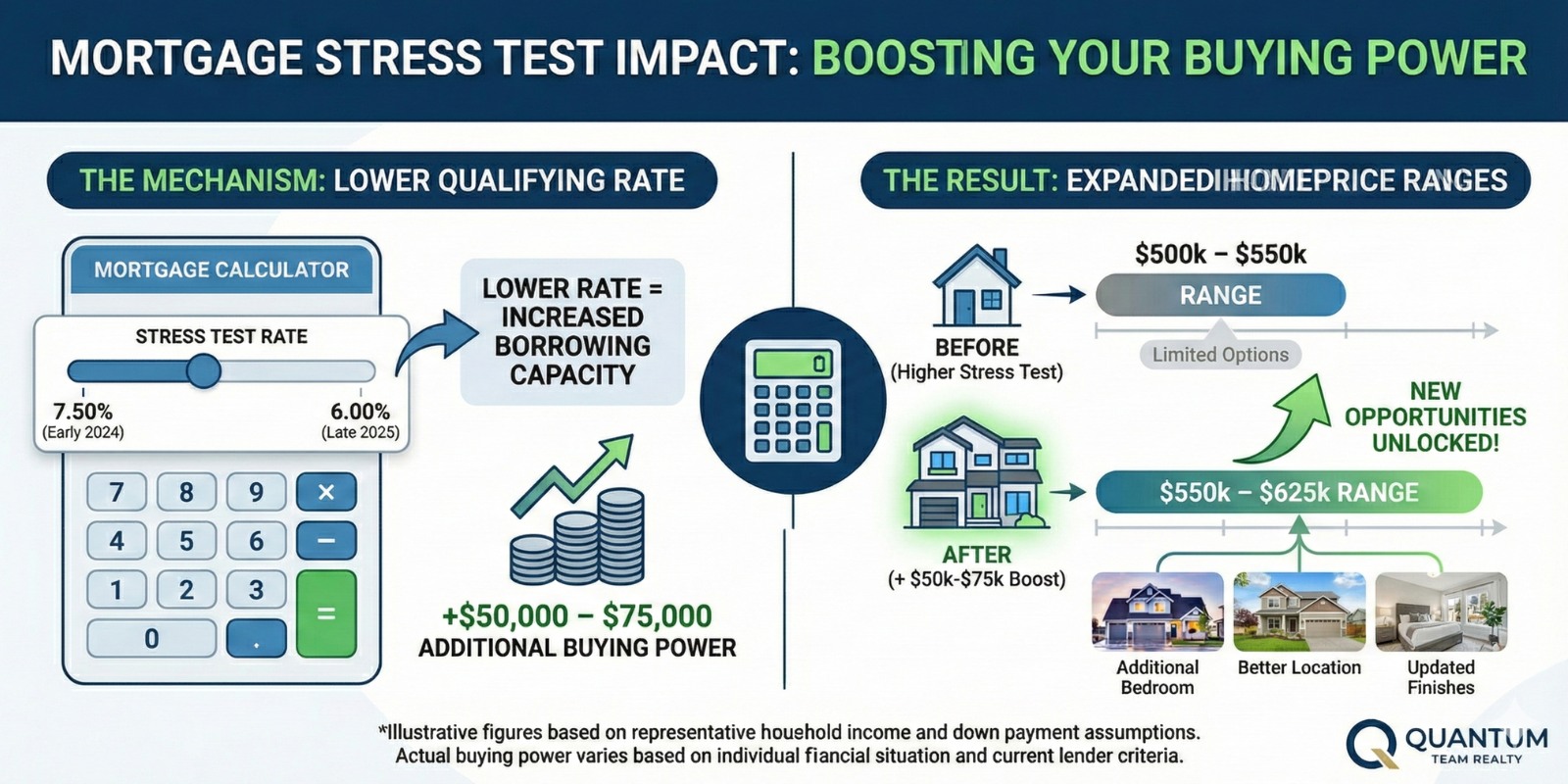

The Stress Test Quietly Improved Affordability

As mortgage rates eased throughout 2024-2025, a secondary effect occurred that received less media attention: qualifying for mortgages became easier.

Canada’s mortgage stress test requires borrowers to qualify at either 5.25% or their contract rate plus 2%—whichever is higher. [OSFI, December 2025]

Stress Test Impact Example:

|

Scenario |

Contract Rate |

Stress Test Rate |

Maximum Mortgage* |

Change in Buying Power |

|---|---|---|---|---|

|

Early 2024 |

5.50% |

7.50% |

$450,000 |

Baseline |

|

Late 2025 |

4.00% |

6.00% |

$500,000 |

+$50,000 (+11%) |

Based on $100,000 household income, 25-year amortization, assuming no other debts

For many Ontario households, the combination of lower contract rates and the resulting lower stress test qualifying rates increased buying power by 50,000–75,000. [Various mortgage calculators, December 2025]

Critically, this improved affordability didn’t reignite speculation because the increased inventory absorbed the additional demand. Supply and demand moved toward balance rather than tipping back into seller-dominated conditions.

- Reset Insight: 2025 improved affordability without reigniting the speculation that caused the problem in the first place.

What 2025 Exposed About the Market

The Stress Test Quietly Improved Affordability

The reset of 2025 revealed structural weaknesses that the frenzied 2021-2022 market had masked:

Solo practitioners struggled when speed no longer mattered more than strategy. Agents who relied on bidding war tactics found themselves unprepared for a market that rewarded patience, accurate pricing, and negotiation skills.

Poor pricing strategies were punished. Sellers who listed 10-15% above comparable sales hoping to “test the market” watched their homes sit unsold while properly priced alternatives moved. According to TRREB data, homes in November 2025 sold for an average of 97% of asking price—meaning the average property sold 3% below list. [WOWA.ca, November 2025]

Experience outweighed optimism. First-time sellers who assumed the market would “always go up” learned painful lessons about market cycles. Meanwhile, experienced real estate professionals who understood fundamentals thrived by guiding clients through realistic expectations.

What the Market Rewarded

At the same time, 2025 validated several strategic approaches:

Team-based brokerages with comprehensive support systems helped clients navigate the complexity of a changing market. At Quantum Team Realty, our multi-location model across Ontario allows us to provide local expertise with broader market insights.

Data-driven pricing replaced emotional pricing. Sellers who worked with agents using comparative market analysis, absorption rates, and real-time inventory tracking sold their homes faster and for better prices than those relying on outdated valuations.

Proactive mortgage planning paid dividends. Homeowners who started renewal conversations 6-12 months before their maturity date secured better rates and avoided renewal shock. With approximately 2.2 million Canadian mortgages scheduled to renew between 2024-2026, early planning separated successful transitions from financial stress. [Bank of Canada analysis, 2024]

Cash-flow-focused investors outperformed speculation-focused investors. As prices stabilized or declined slightly, investors who underwrote properties based on rental income rather than price appreciation maintained stable portfolios.

Why This Was a Reset — Not a Failure

What a Real Market Collapse Looks Like

It’s important to understand what 2025 didn’t experience:

A market collapse includes:

- Forced selling due to widespread defaults

- Credit markets freezing, preventing qualified buyers from accessing mortgages

- Systemic price breakdown (20%+ declines) across all segments

- Panic-driven transactions at any price

2025 showed none of these characteristics.

Mortgage delinquency rates remained historically low. The stress test implemented in 2018 meant most borrowers could absorb payment increases. Credit remained available—banks were actively lending to qualified buyers. And while prices declined moderately, transactions still occurred based on rational pricing rather than distressed selling.

What 2025 Actually Delivered

- Price Discipline: The market punished unrealistic pricing and rewarded accurate valuations. This is healthy market function, not market failure.

- Rate Stability: After years of volatility, the Bank of Canada achieved its dual mandate—inflation near 2% and policy rates in neutral territory. This predictability enabled planning.

- Informed Buyers: First-time buyers entering the 2025 market did so with realistic expectations, proper financing, and understanding of what they could afford. This contrasts sharply with the FOMO-driven purchases of 2021-2022.

- Long-Term Confidence Rebuilding: While transaction volumes remained below peak levels, the buyers and sellers who participated in 2025 did so with greater confidence that they were making sound financial decisions based on fundamentals rather than fear or greed.

Looking Ahead: The Natural Bridge to 2026

What’s Unlikely to Happen

Dramatic rate drops are off the table. With the Bank of Canada signaling it has reached an appropriate policy stance at 2.25%, significant further cuts appear unlikely absent economic deterioration. The next move could be up or down depending on how the economy and inflation evolve. [Bank of Canada, December 2025]

Market-wide price surges won’t return in the near term. The combination of elevated inventory, moderate demand, and affordability constraints creates conditions for gradual price movements rather than rapid appreciation.

What’s More Likely

Selective activity increases in well-priced segments. Quality properties in desirable locations at realistic prices will see strong demand. Poorly priced or lower-quality listings will continue to sit.

Inventory tightening in specific pockets. Some neighborhoods and property types may see supply decline as sellers who can afford to wait choose to hold rather than accept 2025 pricing. This could create micro-markets with competitive conditions even as the broader market remains balanced.

Continued importance of strategy over speed. The days of “list it and watch offers roll in” aren’t returning soon. Success in 2026 will require proper pricing, professional presentation, strategic timing, and skilled negotiation—fundamentals that should have always mattered.

Regional variation intensifying. Ottawa’s +6% price growth in 2025 while Toronto declined 8.2% illustrates how local economic conditions increasingly drive outcomes. [OREA, TRREB, November 2025] This divergence will likely continue as employment patterns, migration trends, and local policies vary across Ontario.

Key Framing Line

“If 2025 was the year the market reset, 2026 will be the year preparation starts paying off.”

Success in 2026 won’t come from timing the market or hoping for rapid appreciation. It will come from understanding the fundamentals, planning properly, and executing with patience and discipline.

Taking Action in the Reset Market

For First-Time Buyers (Ages 25-55)

The reset of 2025 created the most favorable buying conditions for first-time purchasers in half a decade:

Advantages:

- Improved negotiating power with sales-to-listings ratios around 34%

- Ability to include conditions (inspections, financing, home sale) that were impossible in 2021-2022

- Time to conduct due diligence without fear of missing out

- Improved affordability through lower mortgage rates and modest price declines

Action Steps:

- Get pre-approved to understand your purchasing power under current stress test rules (5.25% or rate + 2%)

- Understand first-time buyer incentives available in Ontario

- Work with an experienced agent who can guide you through comparative analysis

- Don’t rush—inventory levels suggest you’ll have options for months ahead

For Current Homeowners Considering Selling

The seller’s experience in 2025-2026 requires different strategies than recent years:

Realities:

- Your home likely won’t sell within days of listing

- Buyers will conduct inspections and may negotiate repairs

- Pricing must be based on recent comparable sales, not neighbor’s 2022 sale price

- Professional presentation matters more when buyers have choices

Action Steps:

- Consult with experienced local agents about realistic pricing based on current inventory and absorption rates

- Invest in home preparation—staging, minor repairs, professional photography

- Be flexible on showing times and conditions

- Consider timing—spring 2026 may see increased activity as rate certainty continues

For Those Facing Mortgage Renewals

With the Bank of Canada policy rate stabilized at 2.25%, those renewing mortgages in 2026 face very different circumstances than those who renewed in 2023-2024:

Current Renewal Environment:

- Fixed rates in the 4% range (down from 5-6% peaks)

- Variable rates around 5.5-6% (prime rate is typically Bank rate + 2%)

- More negotiating power with lenders as competition for quality borrowers increases

Action Steps:

- Start renewal conversations 120-180 days before maturity

- Compare offerings from multiple lenders—your current lender may not offer the best rate

- Consider your household’s risk tolerance when choosing between fixed and variable

- Understand any penalty costs if considering breaking your current mortgage early

What’s the biggest mistake buyers are making right now?

Mistake #1: Waiting for the “perfect” bottom. The market has reset; trying to save an additional 2-3% by waiting could mean missing properties that meet your needs and potentially facing higher rates or prices later.

Mistake #2: Using 2022 sale prices as comparables. That was an anomaly. Current pricing reflects more sustainable fundamentals.

Mistake #3: Skipping pre-approval or assuming affordability based on online calculators. Get properly qualified under current stress test rules to know your true purchasing power.

Partner With Quantum Team Realty

At Quantum Team Realty, we’ve successfully guided Ontario clients through every market condition since our founding. Our multi-location model across Ontario provides both local expertise and regional market insights.

Whether you’re a first-time buyer navigating the reset market, a seller strategizing your approach, or a homeowner planning your mortgage renewal, our experienced team understands the fundamentals that drive successful real estate decisions.

Contact Quantum Team Realty Today

For a personalized market assessment and strategy session tailored to your needs, reach out to our team. In a reset market, preparation and expertise make all the difference.

Visit us at: quantumteamrealty.com

In a reset market, preparation and expertise make all the difference.

Frequently Asked Questions

Will Ontario home prices crash in 2026?

A market crash (20%+ declines, forced selling, credit freeze) remains highly unlikely. Ontario home prices declined 5-8% in 2025—a correction, not a collapse. For 2026, expect continued modest price adjustments in some areas, stabilization in others, and selective strength in markets like Ottawa. The fundamentals supporting Ontario real estate (immigration, job growth, limited new construction) remain intact despite affordability challenges.

Is now a good time to buy in Ontario?

For prepared buyers with stable income and proper financing, the 2025-2026 environment offers the best buying conditions since 2019. Inventory levels above 5 months, sales-to-listings ratios around 34%, and average days on market exceeding 50 days give buyers negotiating power and choice. However, “good time” depends on your personal situation—buying should align with your life circumstances, not market timing alone.

With five-year fixed rates below 4%, many buyers are choosing stability and predictability over variable risk.

What happens if the Bank of Canada raises rates again?

The Bank’s December 2025 statement indicates rates are “about right” at 2.25%, with the next move depending on incoming economic data. If rates do rise (which appears less likely than holds or eventual cuts), it would modestly reduce affordability and could put additional downward pressure on prices. However, the stress test means anyone qualifying today can handle rates approximately 2% higher than their contract rate.

Are bidding wars coming back?

Market-wide bidding wars are unlikely to return soon. However, exceptional properties in desirable locations at competitive prices may still attract multiple offers. The difference from 2021-2022 is that these will be the exception rather than the rule. Most transactions in 2026 will involve negotiation rather than competition.

Should I wait for lower prices before buying?

Trying to “time the bottom” is speculative and may cost more than modest price declines would save. Consider this: if rates decline further, increased demand may push prices up. If rates rise, affordability worsens despite potentially lower prices. Focus instead on: Can you afford the carrying costs? Does it meet your needs? Are you planning to hold long-term? If yes, today’s market conditions are favorable for buyers.

How is Toronto different from the rest of Ontario?

Toronto and the GTA experienced larger price declines (-8% to -10%) than provincial averages in 2025, partly due to starting from higher price points. Toronto also has greater inventory levels and more pronounced buyer’s market conditions. However, Toronto remains Canada’s largest employment center with continued immigration, providing fundamental support despite near-term challenges. Secondary markets like Ottawa showed price growth, illustrating Ontario’s diverse market conditions.

Sunny Chadha

Sunny Chadha is the Co-Founder of Quantum Team Realty and brings over 15 years of experience in Niagara real estate. He is passionate about helping clients make informed decisions and sharing his deep knowledge of the local market.

References

- Bank of Canada. (December 10, 2025). “Bank of Canada maintains policy rate at 2¼%.” Retrieved from bankofcanada.ca

- Bank of Canada. (December 10, 2025). “Summary of Governing Council deliberations: Fixed announcement date of December 10, 2025.” Retrieved from bankofcanada.ca

- Toronto Regional Real Estate Board (TRREB). (November 2025). “Market Watch Report – October 2025.” Retrieved from trreb.ca

- Ontario Real Estate Association (OREA). (November 2025). “Ontario Home Sales Statistics November 2025.” Retrieved from creastats.crea.ca/board/orea

- Niagara Association of REALTORS (NAR). (November 2025). “November 2025 Residential Statistics.” Retrieved from niagararealtor.ca

- WOWA.ca. (November 27, 2025). “Ontario Housing Market Update.” Retrieved from wowa.ca/ontario-housing-market

- WOWA.ca. (December 3, 2025). “Toronto Housing Market Update.” Retrieved from wowa.ca/toronto-housing-market

- nesto.ca. (October 16, 2025). “Toronto Housing Market 2025 Home Prices.” Retrieved from nesto.ca

- nesto.ca. (October 16, 2025). “Ontario Housing Market 2025 Home Prices.” Retrieved from nesto.ca

- Office of the Superintendent of Financial Institutions (OSFI). (2025). “Minimum qualifying rate for uninsured mortgages.” Retrieved from osfi-bsif.gc.ca

- TD Economics. (December 10, 2025). “Why the Bank of Canada just held its interest rate.” TD Stories. Retrieved from stories.td.com

- CBC News. (December 10, 2025). “Bank of Canada holds key interest rate at 2.25%.” Retrieved from cbc.ca/news/business

- Canadian Real Estate Wealth. (May 23, 2025). “Ontario Housing Market Shifts To Buyer’s Market.” Retrieved from canadianrealestatemagazine.ca