When Jennifer and Michael finally saved $140,000 for their “required 20% down payment” on a $700,000 home in Mississauga, they were ready to buy. Then their friend mentioned she’d just purchased a similar home with only $45,000 down. Jennifer was shocked: “Wait, we didn’t need to save 20%?”

In the four extra years it took them to reach 20%, home prices in their target neighborhood increased by $75,000. Their insistence on following outdated advice cost them the opportunity to build equity sooner—and the chance to buy before prices climbed.

Jennifer and Michael’s story isn’t unique. Across Ontario in 2025, thousands of buyers lost opportunities, overpaid, or made poor financial decisions—not because of market conditions, but because they acted on incorrect assumptions. The Ontario real estate market is saturated with advice, much of it outdated or based on market cycles that no longer exist. First-time home buyers are especially vulnerable to common myths that create hesitation, unrealistic expectations, and long-term financial consequences.

This blog separates fact from fiction, examining five costly myths that Ontario buyers must stop believing if they want to make informed real estate decisions in today’s market.

Myth #1: "You Need 20% Down Payment to Buy a Home"

The Truth: You Can Buy with as Little as 5% Down

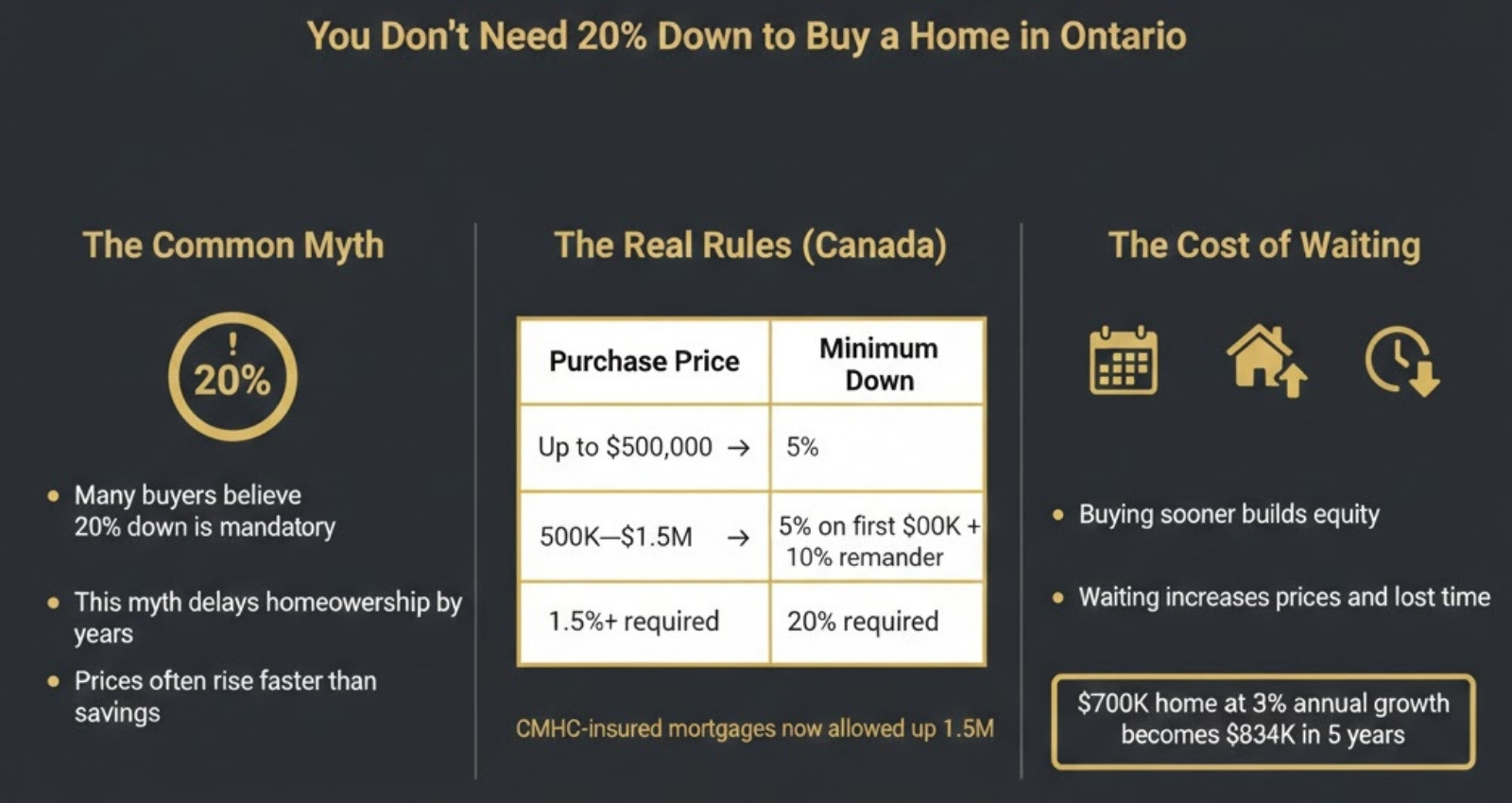

This is perhaps the most damaging myth circulating among first-time Ontario buyers. The reality: Canada’s minimum down payment requirement is 5%—not 20%.

Current Down Payment Requirements in Canada (2026):

| Purchase Price | Minimum Down Payment Required | Example |

|---|---|---|

| Up to $500,000 | 5% of the purchase price | $500,000 home → $25,000 down |

| $500,001 – $1,499,999 | 5% on first $500,000 + 10% on remaining amount | $750,000 home → $50,000 down |

| $1,500,000+ | 20% of the full purchase price | $1,500,000 home → $300,000 down |

- Source: Canada Mortgage and Housing Corporation (CMHC), Government of Canada, 2025-2026

Major Change in December 2024: The federal government increased the CMHC-insured mortgage cap from $1 million to $1.5 million, making it possible for Ontario buyers to purchase homes up to $1.5 million with less than 20% down. This change specifically targets high-cost markets like Toronto and the GTA, where average home prices exceed $1 million.

The Cost of This Myth

Let’s examine what believing this myth costs Ontario buyers:

Scenario: $700,000 Home Purchase

| Period | GTA Average Price | % Change | What Happened |

|---|---|---|---|

| Q4 2024 | $1,106,000 | Baseline | Buyers waiting |

| Q1 2025 | $1,082,000 | -2.2% | “Prices falling, wait more” |

| Q2 2025 | $1,065,000 | -3.7% | “Almost at bottom” |

| Q3 2025 | $1,055,000 | -4.6% | “Just a bit lower” |

| Q4 2025 | $1,039,458 | -6.0% | “Did I miss the bottom?” |

The Hidden Cost: If home prices increase just 3% annually while you save for 20%, that $700,000 home becomes $765,780 in 3 years and $834,305 in 5 years. By waiting, you’re chasing a moving target.

CMHC Mortgage Insurance: Not as Expensive as You Think

Many buyers avoid down payments under 20% because they fear CMHC insurance premiums. Let’s examine the actual math:

- 8% down payment: 4.0% premium on mortgage amount

- 15% down payment: 2.8% premium on mortgage amount

- 19% down payment: 0.6% premium on mortgage amount

For a $700,000 purchase with 10% down ($70,000):

- Mortgage: $630,000

- CMHC Premium (2.8%): $17,640

- Total Mortgage: $647,640

Yes, you’ll pay an additional $17,640 added to your mortgage. But you got into the market 3.5 years sooner, built equity during that time, and locked in today’s prices instead of risking future increases.

Important Note: Ontario charges 8% Retail Sales Tax (RST) on CMHC premiums, which must be paid at closing (cannot be added to mortgage). For the example above, that’s an additional $1,411 cash required.

Action Steps

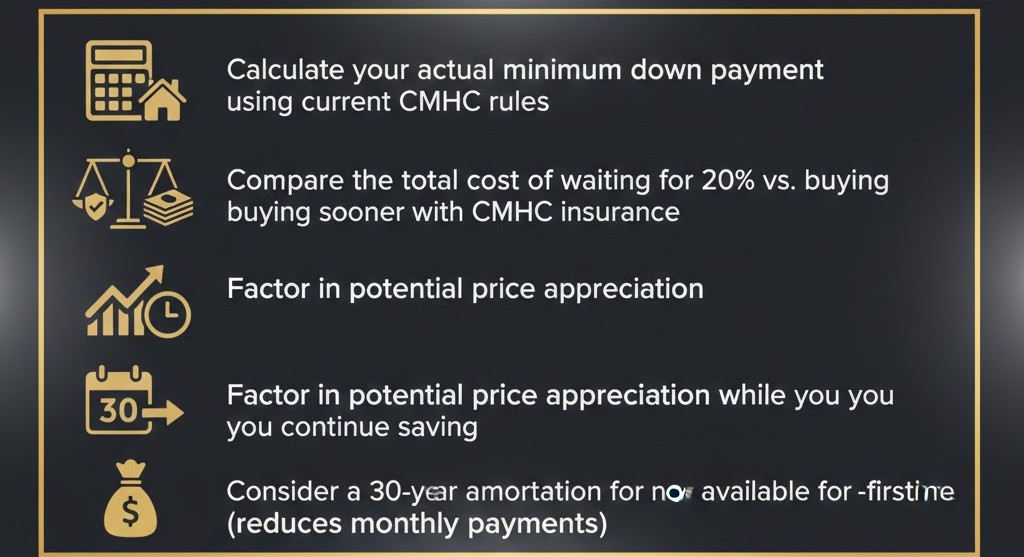

- ✅ Calculate your actual minimum down payment using current CMHC rules

✅ Compare the total cost of waiting for 20% vs. buying sooner with CMHC insurance

✅ Factor in potential price appreciation while you continue saving

✅ Consider a 30-year amortization now available for first-time buyers (reduces monthly payments)

Myth #2: "Waiting for Lower Prices Always Saves You Money"

The Truth: Timing the Market is Nearly Impossible

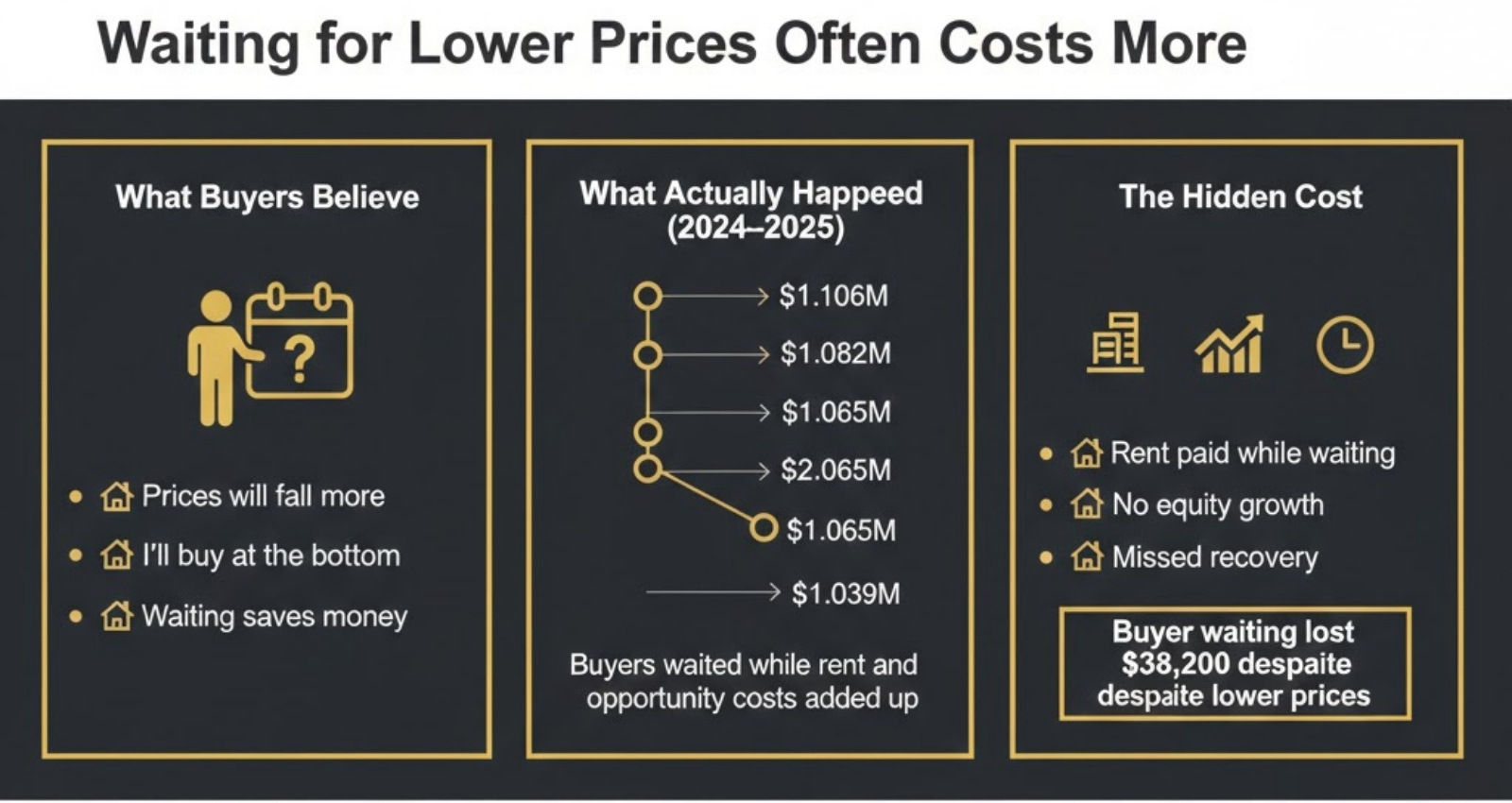

In 2025, many Ontario buyers sat on the sidelines waiting for “the bottom”—that magical moment when prices would hit their lowest point. Here’s what actually happened:

Ontario Housing Price Performance (2024-2025):

| Period | GTA Average Price | % Change | What Happened |

|---|---|---|---|

| Q4 2024 | $1,106,000 | Baseline | Buyers waiting |

| Q1 2025 | $1,082,000 | -2.2% | “Prices falling, wait more” |

| Q2 2025 | $1,065,000 | -3.7% | “Almost at bottom” |

| Q3 2025 | $1,055,000 | -4.6% | “Just a bit lower” |

| Q4 2025 | $1,039,458 | -6.0% | “Did I miss the bottom?” |

- Sources: Toronto Regional Real Estate Board, WOWA.ca, CREA, November 2025

The Waiting Cost Calculator

Example: Buyer waiting for “the perfect bottom” on a $750,000 home

Assumptions:

- Interest rates: 5.5% (early 2024) dropping to 3.8% (late 2025)

- Waiting period: 18 months

- Actual price decline: 6%

| Factor | If Bought Early 2024 | If Waited Until Late 2025 | Difference |

|---|---|---|---|

| Purchase Price | $750,000 | $705,000 ($750K − 6%) | Saved $45,000 |

| Down Payment (10%) | $75,000 | $70,500 | Saved $4,500 |

| Mortgage Rate | 5.5% | 3.8% | Better rate |

| BUT: Lost Equity | Built $40,000+ equity in 18 months | $0 | Lost $40,000 |

| Rent Paid | $0 (living in own home) | $43,200 (18 mo @ $2,400/mo) | Lost $43,200 |

| Net Position | Ahead by $38,200 | Behind | Lost $38,200 |

The buyer who “saved” $45,000 by waiting actually lost $38,200 when accounting for equity buildup, rent payments, and opportunity cost.

What History Teaches Us

Looking at Bank of Canada data, variable-rate mortgages have historically outperformed fixed rates about 85-90% of the time when held for full terms. This suggests that over long periods, market participation beats market timing.

Similarly, real estate appreciation over 10-15 year periods in Ontario has consistently outpaced short-term price fluctuations. The buyers who succeeded weren’t those who timed the market perfectly—they were those who bought when they could afford to and held long-term.

Many buyers avoid down payments under 20% because they fear CMHC insurance premiums. Let’s examine the actual math:

When Waiting Makes Sense

Waiting is smart if:

✅ You’re saving for a larger down payment to avoid CMHC insurance

✅ Interest rates are at historic lows and expected to rise (lock in first)

✅ You need to improve credit score or reduce existing debt

✅ You’re uncertain about employment stability

✅ You haven’t found the right property in your target area

Waiting is costly if:

❌ You’re trying to time “the bottom” of price declines

❌ You’re renting and paying more monthly than potential mortgage costs

❌ Prices are rising faster than you’re saving

❌ You meet all affordability requirements today

Myth #3: "Fixed-Rate Mortgages are Always Safer Than Variable"

The Truth: Variable Rates Often Save Borrowers Money Long-Term

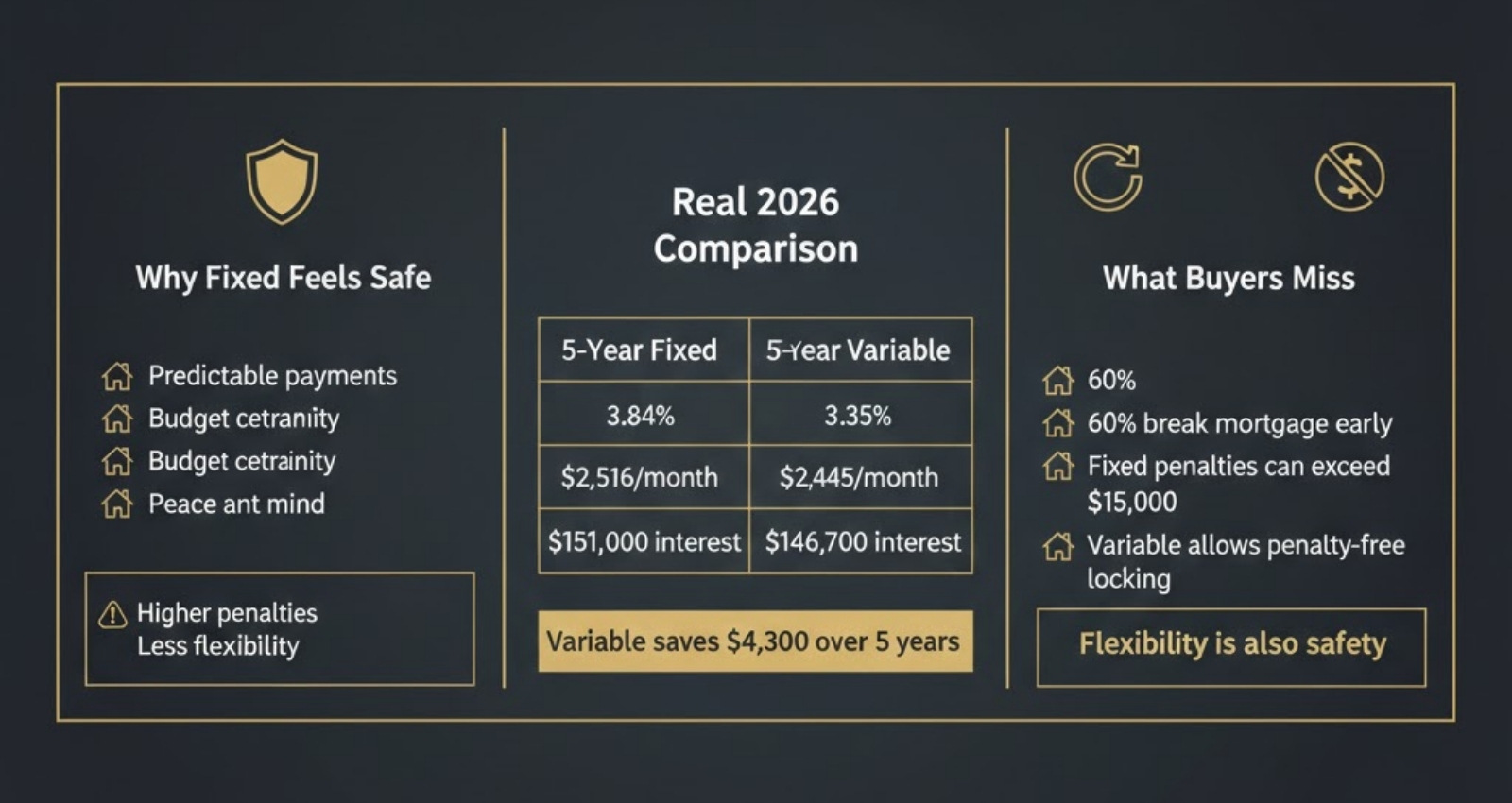

As of January 2026, the best 5-year fixed mortgage rate in Ontario sits around 3.84%, while the best 5-year variable rate is approximately 3.35%—a spread of 0.49%.

This represents one of the narrower gaps in recent years, making the fixed vs. variable decision more nuanced than the conventional wisdom suggests.

Current Ontario Mortgage Rates (January 2026):

| Term & Type | Rate | Monthly Payment on $500K | Total Interest Paid (5 Years) |

|---|---|---|---|

| 5-Year Fixed | 3.84% | $2,516 | $151,000 |

| 5-Year Variable | 3.35% | $2,445 | $146,700 |

| Difference | 0.49% | $71 / month | $4,300 savings |

- Sources: Ratehub.ca, NerdWallet Canada, True North Mortgage, January 2026

The Safety Misconception

Many buyers believe fixed rates are “safer” because payments stay the same. However, fixed rates come with hidden costs:

1. Higher Penalty Costs

If you need to break your mortgage early (selling, refinancing, divorce), penalties differ dramatically:

- Variable mortgage penalty: Typically 3 months’ interest ≈ $4,200 on $500K mortgage

- Fixed mortgage penalty: Interest Rate Differential (IRD) calculation, often $12,000-$20,000+

Approximately 60% of Canadians break their mortgage before the end of their term. The “safety” of fixed rates comes at a steep price if you’re part of that majority.

2. Lower Flexibility

Variable-rate mortgages typically allow you to lock into a fixed rate at any time, penalty-free. Fixed-rate mortgages don’t offer the reverse—you can’t switch to variable without paying the full penalty.

This means variable rates give you optionality. You get the lower rate today with the safety valve of locking in if rates rise significantly.

Historical Performance

A comprehensive study examining Canadian mortgage performance from 1950-2000 (including the volatile high-rate periods of the 1980s and 1990s) found that variable-rate mortgages outperformed fixed rates approximately 85-90% of the time over full 5-year terms.

As of late 2025, with the Bank of Canada holding its overnight rate at 2.25% and signaling a pause, variable rates offer a compelling value proposition. Market forecasts suggest rates will hold through much of 2026, with any increases likely modest (0.25-0.50%) rather than dramatic.

When Fixed Makes Sense

Choose fixed rates if:

✅ You have zero tolerance for payment increases

✅ You’re stretching your budget to qualify

✅ You plan to stay in the home for the full term (no selling/refinancing)

✅ Rates are at historic lows and forecasted to rise substantially

Choose variable rates if:

✅ You can tolerate modest payment fluctuations

✅ You have budget cushion to absorb potential rate increases

✅ You value flexibility and lower penalties

✅ Historical savings and flexibility outweigh payment predictability

Real-World Example: The 2020-2024 Cycle

Buyers who chose variable rates in 2020 (when prime was 2.45%) initially celebrated as rates dropped further to 2.20% in 2021. Then, from 2022-2023, the Bank of Canada executed the fastest tightening cycle in decades, raising rates from 0.25% to 5.0%.

Variable-rate holders faced payment increases of 40-60%. Many panicked and locked into fixed rates near the peak (5.5-6.5%) in late 2023. Those who held their variable rates through 2024-2025 benefited from nine consecutive rate cuts, with prime dropping back to 4.45% by December 2025.

The lesson: short-term volatility doesn’t erase long-term savings, but you need financial resilience to weather the storms.

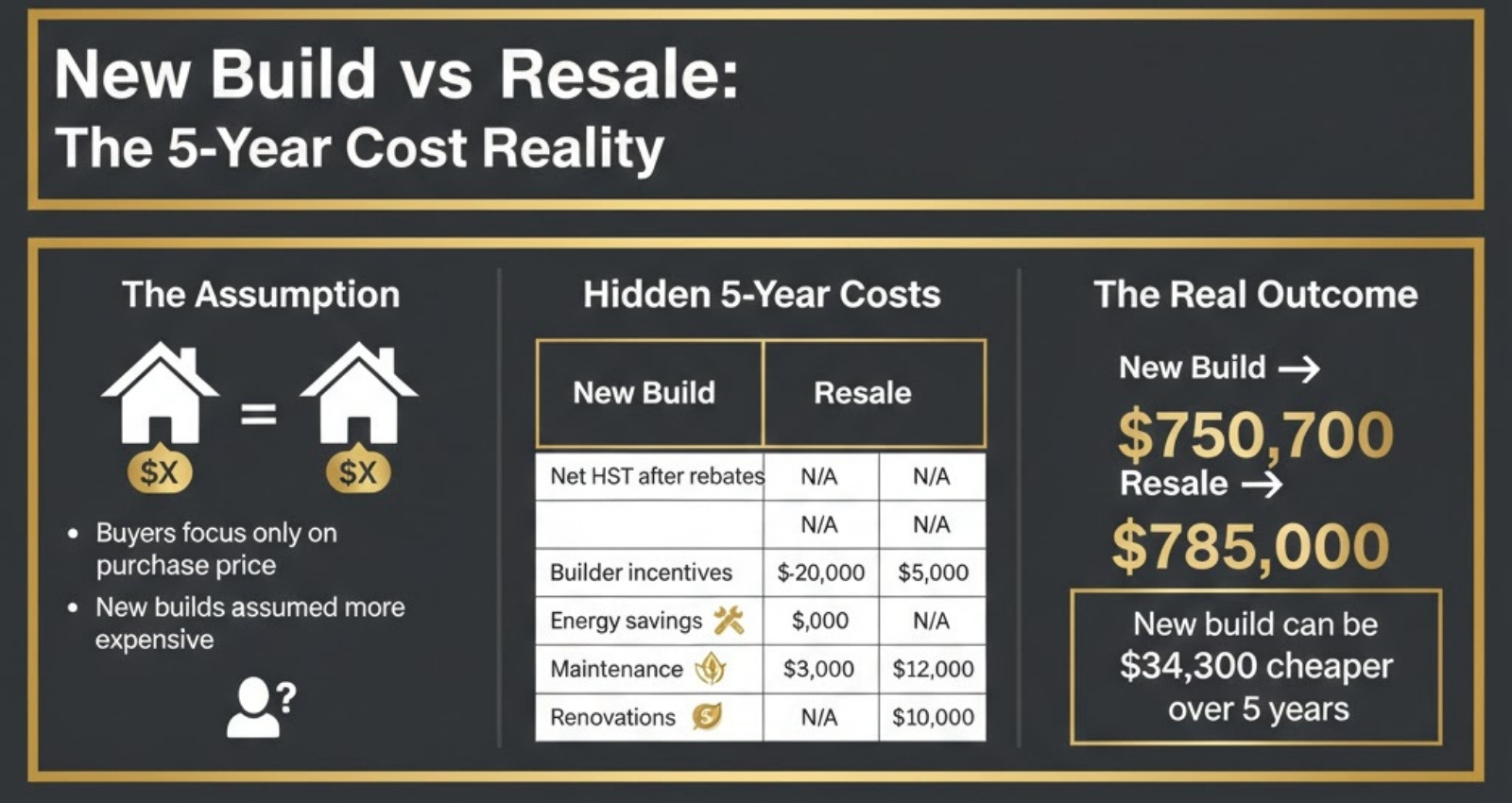

Myth #4: "New Construction Homes Are Always More Expensive Than Resale"

The Truth: The Price Gap is Closing—Sometimes New is Cheaper

Traditionally, new construction commanded a 15-20% premium over comparable resale homes. In 2025-2026, three major shifts are changing this dynamic:

1. Ontario’s New HST Rebate for First-Time Buyers

In late 2025, Ontario introduced a game-changing policy: the province now rebates the full 8% provincial portion of HST on new homes and condos priced up to $1 million for first-time buyers.

HST Savings Breakdown:

| Purchase Price | Provincial HST (8%) | Federal HST (5%) | Federal Rebate | Provincial Rebate | Net HST Owed |

|---|---|---|---|---|---|

| $500,000 — NEW | $40,000 | $25,000 | −$6,300 | −$40,000 | $18,700 |

| $500,000 — RESALE | $0 | $0 | $0 | $0 | $0 |

| Difference | — | Resale $18,700 cheaper | |||

BUT with the new rebate:

| $750,000 NEW (with rebates) | $60,000 | $37,500 | -$6,300 | -$60,000 | $31,200 | | $750,000 RESALE | $0 | $0 | $0 | $0 | $0 |

Wait—that still looks more expensive. Here’s where it gets interesting:

Add in builder incentives (free upgrades worth $15,000-$30,000), closing cost assistance ($5,000-$10,000), and rate buydowns (saving $3,000-$5,000 in year one), and suddenly that $31,200 HST gap shrinks to $0-$10,000.

Now factor in immediate savings:

- Energy costs: New homes use 20-30% less energy (saving $400-$600/year)

- Maintenance costs: $0 in years 1-3 vs. $2,000-$5,000/year for resale homes

- No immediate renovations: Resale homes often need $10,000-$30,000 in updates

Effective 5-Year Total Cost:

| Factor | If Bought Early 2024 | If Waited Until Late 2025 | Difference |

|---|---|---|---|

| Purchase Price | $750,000 | $705,000 ($750K − 6%) | Saved $45,000 |

| Down Payment (10%) | $75,000 | $70,500 | Saved $4,500 |

| Mortgage Rate | 5.5% | 3.8% | Better rate |

| BUT: Lost Equity | Built $40,000+ equity in 18 months | $0 | Lost $40,000 |

| Rent Paid | $0 (living in own home) | $43,200 (18 mo @ $2,400/mo) | Lost $43,200 |

| Net Position | Ahead by $38,200 | Behind | Lost $38,200 |

Sources: Yolevski Real Estate, Defalco Realty, ENERGY STAR, December 2025

2. Resale Homes Often Need Immediate Investment

A 2025 survey found that resale home buyers spent an average of $18,000-$25,000 in the first year on:

- Painting and cosmetic updates

- Appliance replacements

- Roof or HVAC repairs

- Updated flooring

- Bathroom/kitchen modernization

3. Warranty Protection

New homes in Ontario come with Tarion Warranty protection:

- 1 year: Materials and labor

- 2 years: Mechanical systems (plumbing, electrical, heating)

- 7 years: Structural defects

This represents insurance worth thousands that resale homes don’t provide.

When Resale Makes More Sense

Resale homes remain better if:

✅ You need immediate possession (no construction delays)

✅ You want established neighborhoods with mature trees and amenities

✅ You prefer character homes with unique architecture

✅ You can negotiate 10%+ below asking in a buyer’s market

When New Construction Wins

New builds make financial sense if:

✅ You’re a first-time buyer eligible for the HST rebate

✅ Builder incentives offset the initial premium

✅ You value energy efficiency and low maintenance

✅ You’re buying in a growth area with infrastructure improvements

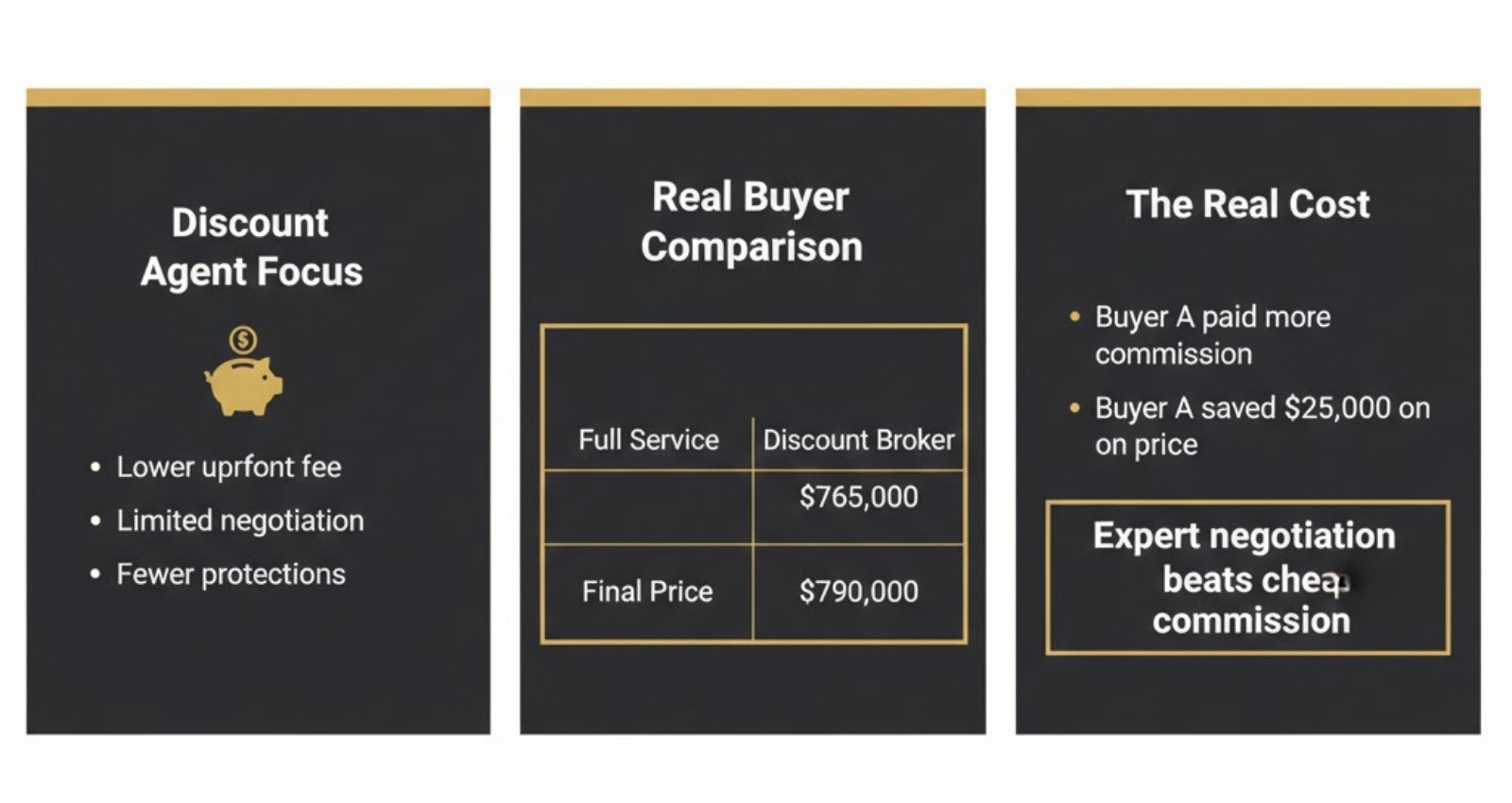

Myth #5: "All Real Estate Agents Offer the Same Value"

The Truth: Agent Quality Dramatically Impacts Your Final Cost

In 2025, Ontario buyers who worked with experienced, full-service teams paid an average of $12,000-$18,000 less than buyers who chose discount brokers or solo agents based on commission savings alone.

Real-World Example: Two $800,000 Home Purchases

| Purchase Price | Provincial HST (8%) | Federal HST (5%) | Federal Rebate | Provincial Rebate | Net HST Owed |

|---|---|---|---|---|---|

| $500,000 — NEW | $40,000 | $25,000 | −$6,300 | −$40,000 | $18,700 |

| $500,000 — RESALE | $0 | $0 | $0 | $0 | $0 |

| Difference | — | Resale $18,700 cheaper | |||

Buyer A “paid more in commission” but saved $25,000 on purchase price. Buyer B “saved on commission” but overpaid by $25,000.

Net difference: Buyer A is ahead by $13,000 despite paying double the commission.

What Full-Service Agents Provide

1. Market Expertise

- Access to off-market listings

- Accurate pricing guidance (avoiding overpayment)

- Knowledge of upcoming inventory

- Understanding of neighborhood micro-trends

2. Negotiation Skills

- In Toronto’s 2025 market, homes sold for an average of 97% of asking price

- Experienced agents consistently negotiate 2-5% better outcomes

- On a $750,000 purchase, that’s $15,000-$37,500 in savings

3. Due Diligence

- Identifying property red flags during viewings

- Coordinating professional inspections

- Reviewing status certificates (condos)

- Title searches and legal issue identification

4. Transaction Management

- Coordinating lawyers, lenders, inspectors

- Managing conditional periods

- Ensuring smooth closing process

- Problem-solving when issues arise

5. Post-Purchase Support

- Contractor referrals

- Mortgage renewal guidance

- Future sale planning

- Market updates

The $12,000 Question

Would you rather:

- Save $5,000 on commission and potentially overpay $20,000 on purchase price?

- Pay standard commission and save $20,000-$30,000 through expert negotiation and market knowledge?

The answer is obvious—yet thousands of Ontario buyers choose the former every year.

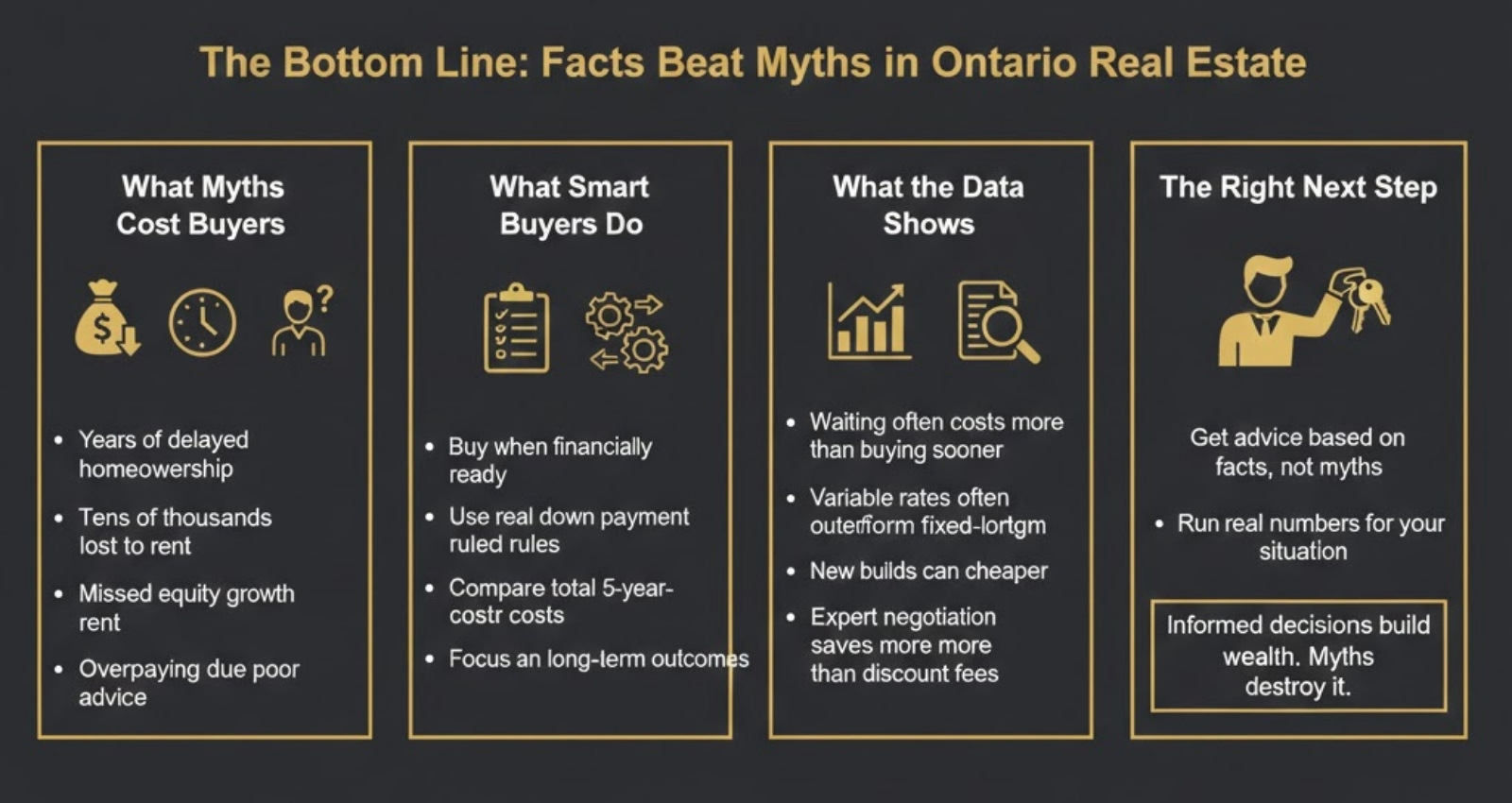

The Bottom Line: Separating Fact from Fiction in Ontario Real Estate

Real estate myths persist because they contain kernels of truth—then get distorted through repetition until they become harmful oversimplifications. The myth that you need 20% down was once practical advice when mortgage insurance didn’t exist. Now it prevents qualified buyers from building equity years sooner. The belief that fixed mortgages are always safer ignores historical data showing variable rates typically save money. The assumption that new construction is always more expensive overlooks recent policy changes making new builds competitively priced.

What costs Ontario buyers thousands isn’t bad luck or market timing—it’s operating on outdated assumptions instead of current facts. The buyers who succeed in 2026 will be those who:

✅ Understand actual down payment minimums and run the real math

✅ Buy when they’re financially ready instead of trying to time market bottoms

✅ Evaluate fixed vs. variable based on their situation and risk tolerance, not conventional wisdom

✅ Compare total 5-year costs of new vs. resale, not just purchase price

✅ Choose real estate partners based on expertise and results, not commission discounts

Every one of these myths has cost real Ontario buyers real money in the past year. Don’t let 2026 be the year you make the same expensive mistakes.

Partner With Quantum Team Realty

At Quantum Team Realty, we help Ontario buyers navigate real estate decisions with facts, data, and proven strategies—not myths and outdated advice. Our experienced team has guided hundreds of first-time buyers through successful purchases, often saving them thousands through expert negotiation and market insight.

Whether you’re determining your actual minimum down payment, deciding between fixed and variable rates, comparing new construction and resale options, or simply want guidance from professionals who understand today’s Ontario market, we’re here to help.

Contact Quantum Team Realty today for a personalized consultation. We’ll help you separate fact from fiction and make confident real estate decisions based on your unique situation.

Stop believing costly myths. Start building wealth through informed homeownership.

Frequently Asked Questions

Can I really buy a home in Ontario with only 5% down?

Yes. For properties under $500,000, you need only 5% down. For properties $500,000-$1.5 million, you need 5% on the first $500,000 and 10% on the remainder. This makes homeownership accessible much sooner than saving for 20%. You’ll need CMHC insurance, but the cost is added to your mortgage and the monthly impact is often less than rent.

What if home prices drop after I buy?

Short-term price fluctuations are normal and shouldn’t drive buying decisions if you’re holding long-term (7+ years). Ontario real estate has consistently appreciated over 10-15 year periods. If you have stable income, bought within your budget, and plan to stay, temporary dips are irrelevant. Focus on whether homeownership meets your life needs, not market timing.

How do I know if variable or fixed rate is right for me?

Start by asking: Can I afford a 1% rate increase? If yes, variable offers better long-term savings and flexibility. If no, fixed provides payment certainty. Also consider your plans—if there’s any chance you’ll sell or refinance in 3-4 years, variable’s lower penalties make it attractive even if rates rise moderately.

Should I buy new construction or resale right now?

If you’re a first-time buyer, Ontario’s new 8% HST rebate (effective late 2025) dramatically improves new construction affordability. Add builder incentives and long-term energy savings, and new builds can be financially competitive or superior. However, if you need immediate possession or want an established neighborhood, resale remains the better choice. Evaluate both options with total 5-year cost in mind, not just sticker price.

How much do real estate agents actually impact my final price?

Significantly. Data shows experienced agents negotiate outcomes 2-5% better than average, which on a $700,000 purchase equals $14,000-$35,000 in savings. They also prevent costly mistakes (buying homes with hidden issues, missing crucial deadlines, accepting unfavorable conditions). The commission you pay is more than offset by negotiation savings and risk avoidance.

Is now a good time to buy in Ontario?

For prepared buyers with stable income and proper financing, 2025-2026 offers excellent conditions: interest rates have declined from 2023-2024 peaks, inventory levels are elevated (giving buyers choice and negotiation power), and prices have moderated 6-8% from all-time highs. However, “good time” is personal—buy when homeownership aligns with your life plans and budget, not because you’re trying to time a market bottom.

What's the biggest mistake Ontario first-time buyers make?

Believing they need 20% down payment and waiting years to reach it. During those years, home prices often rise faster than savings grow, making homeownership perpetually out of reach. The second biggest mistake is choosing a real estate agent based solely on commission percentage rather than expertise and proven results.

Sunny Chadha

Sunny Chadha is the Co-Founder of Quantum Team Realty and brings over 15 years of experience in Niagara real estate. He is passionate about helping clients make informed decisions and sharing his deep knowledge of the local market.

References

- Canada Mortgage and Housing Corporation (CMHC). (2025). “Homeowner Mortgage Loan Insurance Requirements.” Retrieved from cmhc-schl.gc.ca

- Government of Canada. (2025). “How much you need for a down payment.” Retrieved from canada.ca

- WOWA.ca. (2026). “CMHC Mortgage Rules 2026.” Retrieved from wowa.ca/cmhc-mortgage-rules

- Findlay Real Estate. (December 11, 2024). “Canada’s New Mortgage Rules 2025: What Homebuyers Need to Know.” Retrieved from findlayrealestate.ca

- Ratehub.ca. (January 29, 2026). “Best mortgage rates Canada.” Retrieved from ratehub.ca/best-mortgage-rates

- NerdWallet Canada. (December 2025). “Mortgage Rates Ontario.” Retrieved from nerdwallet.com/ca

- True North Mortgage. (January 2026). “Should you choose a variable rate in 2026?” Retrieved from truenorthmortgage.ca

- Altrua Financial. (December 18, 2025). “Variable vs Fixed Mortgage Canada: Ultimate Guide in 2025-2026.” Retrieved from altrua.ca

- nesto.ca. (December 12, 2025). “Fixed vs Variable Mortgage Rates.” Retrieved from nesto.ca

- Toronto Regional Real Estate Board (TRREB). (November 2025). “Market Statistics.” Retrieved from trreb.ca

- WOWA.ca. (November 27, 2025). “Ontario Housing Market Update.” Retrieved from wowa.ca/ontario-housing-market

- Yolevski Real Estate. (October 30, 2025). “Ontario’s New HST Rebate Is a Game Changer for First-Time Home Buyers.” Retrieved from yolevski.com

- Defalco Realty. (July 11, 2025). “New Construction vs Resale Home: Pros & Cons 2025 Guide.” Retrieved from defalcorealty.com

- Matt Richling. (May 2, 2025). “Should You Buy a New Build Condo or a Resale? The 2025 Ottawa Edition.” Retrieved from mattrichling.com

- RE/MAX. (December 23, 2025). “Buying New Construction vs. Resale Homes.” Retrieved from blog.remax.com