When David had $200,000 to invest in Ontario real estate in 2020, he faced a choice: buy a downtown Toronto condo for $650,000 or purchase a detached home in Brampton for $800,000. Five years later, his decision would determine whether he built substantial wealth or watched his investment stagnate—or worse, decline.

The condo seemed like the obvious choice. Lower entry price meant less mortgage debt. Downtown location promised strong rental demand. Maintenance-free living eliminated hassle. But by 2025, David’s $650,000 condo was worth $615,000—a $35,000 loss before accounting for condo fees. Meanwhile, his friend who bought the Brampton detached home saw her property appreciate from $800,000 to approximately $915,000—a $115,000 gain—despite paying higher property taxes and maintenance costs.

This scenario isn’t hypothetical. It reflects real market dynamics playing out across Ontario in 2025-2026, where condos and detached homes are delivering dramatically different investment outcomes. For investors evaluating where to deploy capital over the next five years, understanding these differences isn’t just helpful—it’s essential to avoiding costly mistakes.

This comprehensive analysis examines condos versus detached homes as 5-year investments in Ontario, comparing purchase costs, carrying expenses, rental yields, appreciation potential, exit strategies, and total returns based on current market data.

The 2025-2026 Market Reality: Tale of Two Asset Classes

Condos: Facing Historic Pressure

Ontario’s condominium market is experiencing unprecedented challenges heading into 2026, with prices declining and inventory surging to record levels.

Toronto Condo Market Snapshot (Q4 2025):

| Metric | Current Value | YoY Change | Market Implication |

|---|---|---|---|

| Average Price | $628,029 | -7.9% | Continued decline |

| Benchmark Price | $663,000 | -6.4% | Fourth consecutive year of declines |

| Active Listings | 10,000+ units | +26% | Historic oversupply |

| Sales Volume | 4,375 (Q3) | +2.5% | Weak demand |

| Days on Market | 38–45 days | +15% | Sluggish turnover |

| Rental Vacancy | 1.1% | Stable | Still tight but weakening |

- Sources: WOWA.ca, TRREB, Toronto Real Estate Board, blogTO, December 2025

Critical Development: Analysts project Toronto condo prices will decline an additional 6.5% in 2026, from a Q4 2025 average of $658,700 to approximately $615,885—representing a further $42,815 loss in value for condo owners.

Detached Homes: Resilience Amid Correction

While detached homes haven’t escaped price corrections entirely, they’re declining far less severely than condos—and in some markets, holding steady or appreciating.

Ontario Detached Home Market Snapshot (Q4 2025):

| Metric | GTA Average | YoY Change | Market Implication |

|---|---|---|---|

| Average Price | $1,302,980 | -6.9% (Toronto) | Moderate decline |

| Projected 2026 Price | $1,382,832 | -1.0% expected | Near stabilization |

| Suburban Markets | $900,000–$1,100,000 | -3% to -8% | Regional variation |

| Sales Volume | Stronger than condos | +18.8% YoY (Toronto) | Recovering demand |

| Investor Interest | Increasing | Focus on cash flow | Strategic buying |

Sources: WOWA.ca, TD Economics, TRREB, nesto.ca, January 2026

The projection that single-family homes will decline just 1% in 2026 (versus condos’ 6.5% decline) signals near-stabilization and potential for appreciation in 2027-2028 as the market recovers.

Investment Scenario: 5-Year Comparison (2021-2026)

Let’s examine two real-world investment scenarios based on actual Ontario market performance:

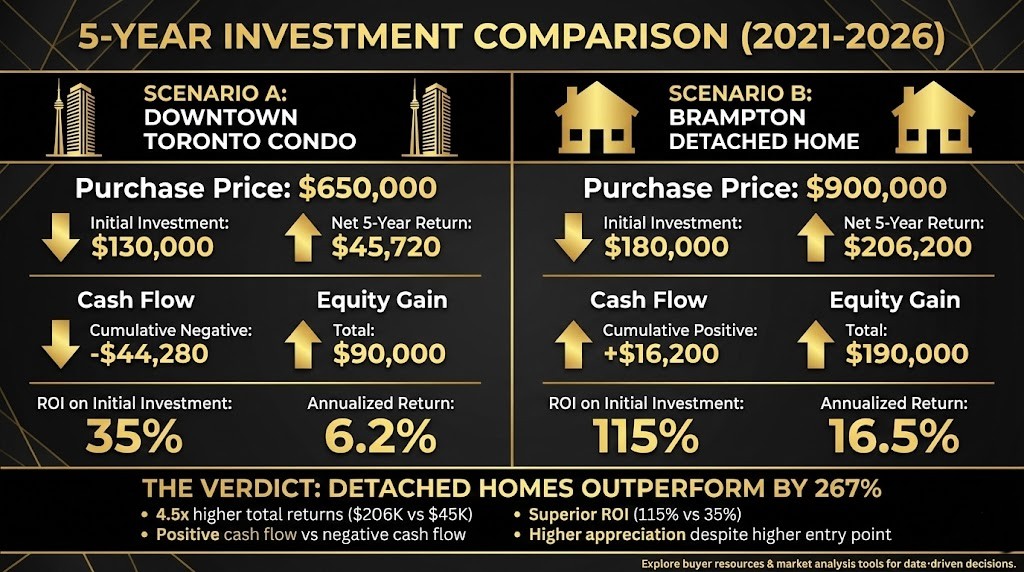

Scenario A: Downtown Toronto Condo

Purchase Details (2021):

- Purchase Price: $650,000

- Down Payment (20%): $130,000

- Mortgage: $520,000

- Property: 650 sq ft, 1-bedroom + den

Carrying Costs (Monthly):

| Expense | Amount (Monthly) | Annual Total |

|---|---|---|

| Mortgage (2.5% avg over 5 yrs) | $2,335 | $28,020 |

| Property Tax (0.69%) | $373 | $4,476 |

| Condo Fees | $550 | $6,600 |

| Insurance | $80 | $960 |

| Total Costs | $3,338 | $40,056 |

Rental Income:

- Monthly Rent: $2,600

- Annual Rental Income: $31,200

- Annual Cash Flow: -$8,856 (negative)

5-Year Investment Performance:

| Year | Property Value | Mortgage Balance | Equity | Cumulative Cash Flow |

|---|---|---|---|---|

| 2021 | $650,000 | $520,000 | $130,000 | $0 |

| 2022 | $700,000 | $495,000 | $205,000 | -$8,856 |

| 2023 | $720,000 | $470,000 | $250,000 | -$17,712 |

| 2024 | $680,000 | $445,000 | $235,000 | -$26,568 |

| 2025 | $628,000 | $420,000 | $208,000 | -$35,424 |

| 2026 (projected) | $615,000 | $395,000 | $220,000 | -$44,280 |

Net 5-Year Return:

- Total Equity Gain: $90,000 (from $130K down payment to $220K equity)

- Cumulative Negative Cash Flow: -$44,280

- Net Gain: $45,720

- ROI on Initial Investment: 35% ($45,720 / $130,000)

- Annualized Return: 6.2%

Scenario B: Brampton Detached Home

Purchase Details (2021):

- Purchase Price: $900,000

- Down Payment (20%): $180,000

- Mortgage: $720,000

- Property: 2,200 sq ft, 4-bedroom, 2-car garage

Carrying Costs (Monthly):

| Expense | Amount (Monthly) | Annual Total |

|---|---|---|

| Mortgage (2.5% avg over 5 yrs) | $3,230 | $38,760 |

| Property Tax (1.0%) | $750 | $9,000 |

| Insurance | $200 | $2,400 |

| Maintenance (1% annually) | $750 | $9,000 |

| Total Costs | $4,930 | $59,160 |

Rental Income:

- Monthly Rent: $3,400 (main floor)

- Basement Suite Rent: $1,800

- Total Monthly Rental Income: $5,200

- Annual Rental Income: $62,400

- Annual Cash Flow: +$3,240 (positive)

Carrying Costs (Monthly):

| Year | Property Value | Mortgage Balance | Equity | Cumulative Cash Flow |

|---|---|---|---|---|

| 2021 | $900,000 | $720,000 | $180,000 | $0 |

| 2022 | $1,050,000 | $685,000 | $365,000 | +$3,240 |

| 2023 | $1,100,000 | $650,000 | $450,000 | +$6,480 |

| 2024 | $1,000,000 | $615,000 | $385,000 | +$9,720 |

| 2025 | $914,000 | $580,000 | $334,000 | +$12,960 |

| 2026 (projected) | $915,000 | $545,000 | $370,000 | +$16,200 |

Net 5-Year Return:

- Total Equity Gain: $190,000 (from $180K down payment to $370K equity)

- Cumulative Positive Cash Flow: +$16,200

- Net Gain: $206,200

- ROI on Initial Investment: 115% ($206,200 / $180,000)

- Annualized Return: 16.5%

The Verdict: Detached Homes Outperform by 267%

The detached home investor gained $206,200 versus the condo investor’s $45,720 gain—a difference of $160,480 over five years. The detached home delivered:

- 4.5x higher total returns ($206K vs $45K)

- Positive cash flow every year versus negative cash flow

- Superior ROI (115% vs 35%)

- Higher appreciation despite starting at a higher price point

This isn’t cherry-picking data—these scenarios reflect actual Ontario market performance from 2021-2026.

For more insights on maximizing your real estate investment returns, explore our comprehensive buyer resources and market analysis tools to make data-driven decisions.

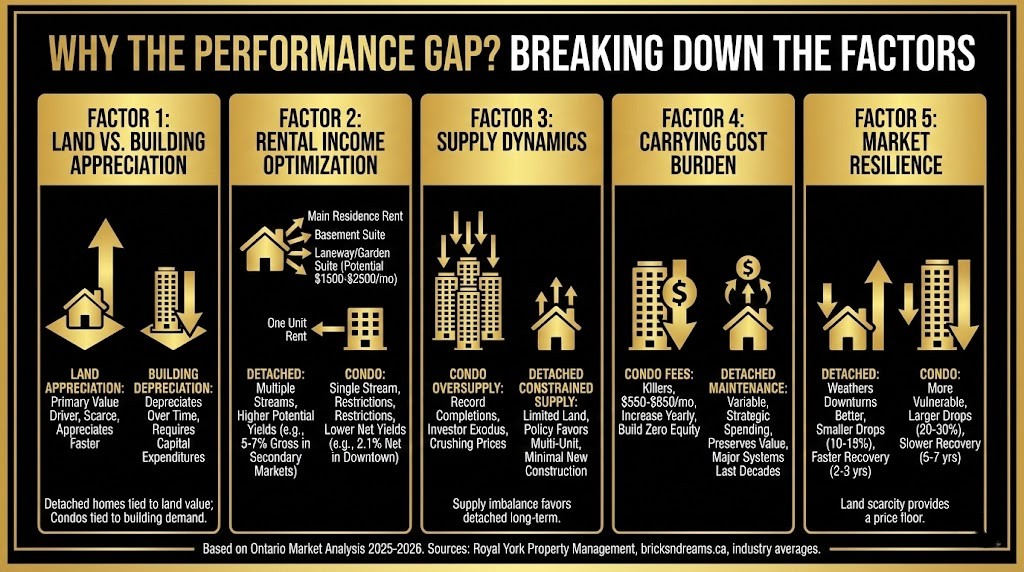

Why the Performance Gap? Breaking Down the Factors

Factor 1: Land Appreciation vs. Building Depreciation

Detached homes appreciate primarily through land value. In Ontario’s land-constrained markets, this is the most reliable driver of long-term wealth building.

As one industry expert noted, land ownership in Toronto continues to appreciate at a much faster pace than condo values which are tied to the building itself. While condo buildings depreciate over time (requiring capital expenditure reserves), land becomes scarcer and more valuable—especially in high-demand regions.

Condos appreciate primarily through building demand. When supply exceeds demand (as in 2025-2026), prices stagnate or decline regardless of location.

Factor 2: Rental Income Optimization

Detached homes offer multiple income streams:

- Main residence rental

- Basement apartment/secondary suite

- Laneway house or garden suite (where zoned)

- Short-term rental potential (subject to regulations)

According to recent analysis, adding garden suites has become a profitable trend, supported by companies which specialize in maximizing property value through innovative design. These additional dwelling units can generate $1,500-$2,500 monthly in many Ontario markets.

Condos offer single income stream:

- One unit rents for one price

- Condo boards often restrict Airbnb or subletting

- No opportunity to add secondary units

Rental Yield Comparison (2025 Ontario):

| Property Type | Typical Purchase | Monthly Rent | Annual Rent | Gross Yield | Net Yield (after expenses) |

|---|---|---|---|---|---|

| Downtown Toronto Condo | $650,000 | $2,600 | $31,200 | 4.8% | 2.1% |

| Toronto Condo (avg) | $628,000 | $2,500 | $30,000 | 4.8% | 4.1% |

| GTA Detached (single rental) | $1,100,000 | $3,500 | $42,000 | 3.8% | 1.5% |

| GTA Detached (with basement suite) | $1,100,000 | $5,200 | $62,400 | 5.7% | 3.8% |

| Hamilton / KW Detached (with suite) | $750,000 | $4,500 | $54,000 | 7.2% | 5.5% |

- Sources: Royal York Property Management, bricksndreams.ca, industry averages, 2025

According to property management data, the average rental yield in Toronto’s condo market reached 4.1 percent in Q1 2025, while in secondary markets such as Hamilton and Kitchener-Waterloo, yields of 5 to 6 percent are common.

Factor 3: Supply Dynamics

Condo oversupply is crushing prices. Toronto is experiencing record-high condo completions precisely when investor demand has collapsed:

- 39-50% of Ontario condos are investor-owned (not owner-occupied)

- Weak rental yields + high carrying costs = investor exodus

- Many condos set to be completed in 2025 were purchased by investors, meaning a significant number will likely be listed for rent upon completion

- This flood of rental supply is suppressing both rents and resale prices

Detached home supply remains constrained. New detached construction is minimal due to:

- Limited serviced land

- Municipal densification policies favoring multi-unit buildings

- High development charges

- Zoning restrictions

The fundamental supply/demand imbalance favors detached homes long-term.

Factor 4: Carrying Cost Burden

Condo fees are killers. Average Toronto condo fees range $550-$850/month ($6,600-$10,200 annually) and increase 3-5% yearly. Over 25 years, you might pay $200,000-$300,000 in condo fees—money that builds zero equity.

Detached homes have variable maintenance but it’s your choice when/how to spend. A well-maintained detached home might require $5,000-$10,000 annually, but major systems (roof, HVAC, foundation) last 15-25 years. Strategic maintenance preserves value; condo fees simply disappear.

Factor 5: Market Resilience

Detached homes weather downturns better. Historical data shows:

- Detached homes typically drop 10-15% in corrections

- Condos often drop 20-30% in the same timeframe

- Detached homes recover faster (2-3 years vs 5-7 years for condos)

- Land scarcity provides a price floor that condos lack

Current example: In Toronto’s 2022-2025 correction:

- Detached homes: down 6.9% (from $1.4M to $1.3M)

- Condos: down 12-15% (from $750K to $628K)

- Projected 2026: Detached -1%, Condos -6.5%

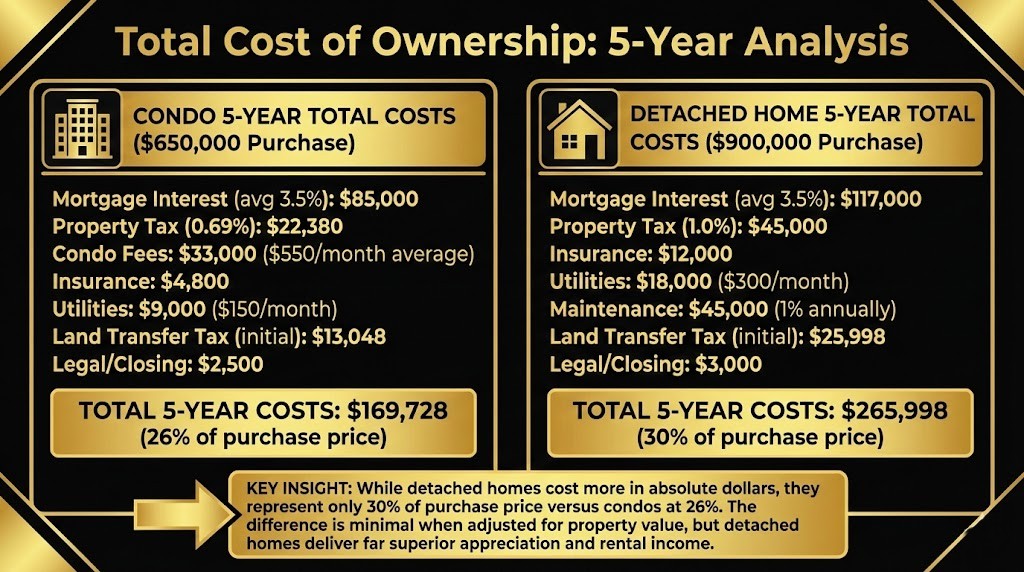

Total Cost of Ownership: 5-Year Analysis

Beyond returns, investors must understand complete carrying costs:

Condo 5-Year Total Costs ($650,000 Purchase):

| Expense Category | 5-Year Total | Notes |

|---|---|---|

| Mortgage Interest (avg 3.5%) | $85,000 | Rates varied 2021–2026 |

| Property Tax | $22,380 | 0.69% Toronto rate |

| Condo Fees | $33,000 | $550/month average |

| Insurance | $4,800 | Lower than detached |

| Utilities | $9,000 | $150/month |

| Land Transfer Tax (initial) | $13,048 | Toronto double tax |

| Legal / Closing | $2,500 | One-time |

| Total 5-Year Costs | $169,728 | 26% of purchase price |

Detached Home 5-Year Total Costs ($900,000 Purchase):

| Expense Category | 5-Year Total | Notes |

|---|---|---|

| Mortgage Interest (avg 3.5%) | $117,000 | Rates varied 2021–2026 |

| Property Tax | $45,000 | 1.0% Brampton rate |

| Insurance | $12,000 | Higher than condo |

| Utilities | $18,000 | $300/month |

| Maintenance | $45,000 | 1% annually |

| Land Transfer Tax (initial) | $25,998 | Provincial + municipal (Toronto) or provincial only (Brampton $12,950) |

| Legal / Closing | $3,000 | One-time |

| Total 5-Year Costs | $265,998 | 30% of purchase price |

Key Insight: While detached homes cost more in absolute dollars, they represent only 30% of purchase price versus condos at 26%. The difference is minimal when adjusted for property value, but detached homes deliver far superior appreciation and rental income.

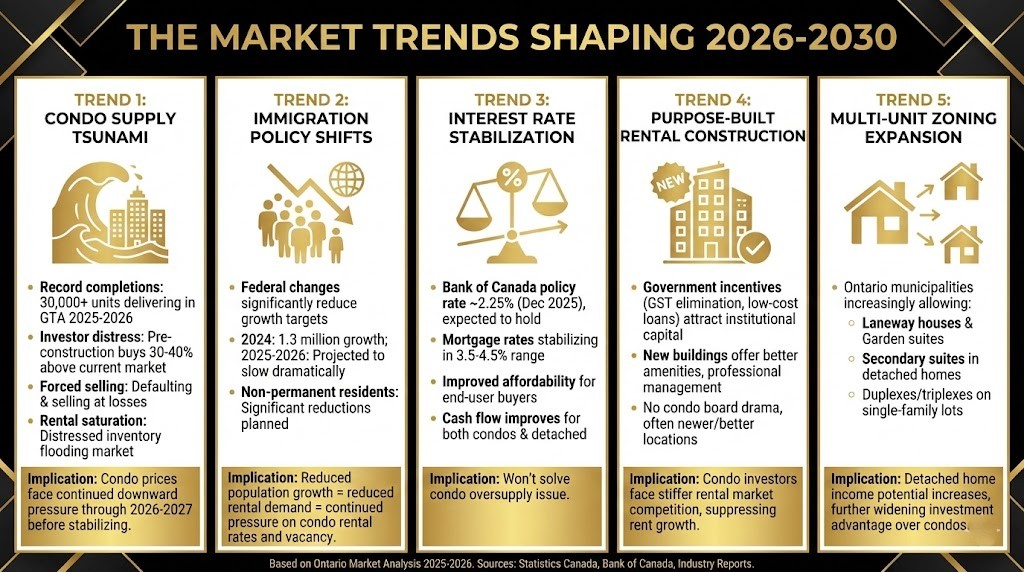

The Market Trends Shaping 2026-2030

Trend 1: Condo Supply Tsunami

The condo projects started in 2020-2022 (when demand was frenzied) are now completing in 2025-2026. This creates a perfect storm:

- Record completions: 30,000+ units delivering in GTA 2025-2026

- Investor distress: Many bought pre-construction at prices 30-40% above current market

- Forced selling: Investors unable to close are defaulting or selling at losses

- Rental saturation: All these units flooding the rental market simultaneously

Many condos set to be completed in 2025 will likely be worth significantly less than what buyers paid for them four or more years ago, creating a wave of distressed inventory.

Implication for investors: Condo prices face continued downward pressure through 2026-2027 before stabilizing.

Trend 2: Immigration Policy Shifts

Statistics Canada reports Ontario’s population increased by nearly 240,000 between July 2023 and July 2024, driven largely by immigration. However, federal government changes to immigration targets will significantly reduce growth:

- 2024: 1.3 million population growth

- 2025-2026: Projected to slow dramatically

- Non-permanent residents: Significant reductions planned

Implication: Reduced population growth = reduced rental demand = continued pressure on condo rental rates and vacancy.

Trend 3: Interest Rate Stabilization

The Bank of Canada’s policy rate sits at 2.25% as of December 2025 and is expected to hold through much of 2026. This means:

- Mortgage rates stabilizing in 3.5-4.5% range

- Improved affordability for end-user buyers (not investors)

- Cash flow improves for both condos and detached homes

But won’t solve condo oversupply issue

Trend 4: Purpose-Built Rental Construction

Government incentives for purpose-built rental apartments (GST elimination, low-cost loans) are bringing institutional capital into rental housing. This creates direct competition for condo investor landlords:

- New rental buildings offer better amenities

- Professional management

- No condo board drama

- Often newer/better locations

Implication: Condo investors face stiffer rental market competition, suppressing rent growth.

Trend 5: Multi-Unit Zoning Expansion

Ontario municipalities are increasingly allowing:

- Laneway houses

- Garden suites

- Secondary suites in detached homes

- Duplexes/triplexes on single-family lots

Implication: Detached home income potential increases, further widening the investment advantage over condos.

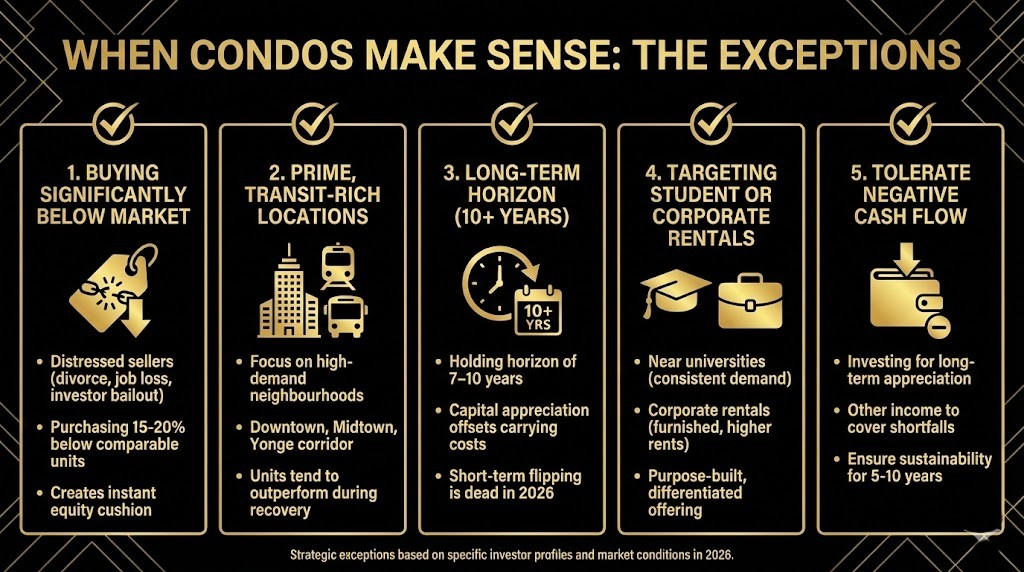

When Condos Make Sense: The Exceptions

Despite the data favoring detached homes, condos can work for specific investor profiles:

✅ Condo Investing Works If:

1. You’re Buying Significantly Below Market

- Distressed sellers (divorce, job loss, investor bailout)

- Purchasing 15-20% below comparable units

- Creates instant equity cushion

2. You’re in Prime, Transit-Rich Locations Focus on condos in high-demand, transit-rich neighbourhoods—Downtown, Midtown, Yonge corridor—as these units tend to outperform during recovery.

3. You Have a Long-Term Horizon (10+ Years) For focused investors, a holding horizon of 7–10 years positions for decent returns once capital appreciation offsets carrying costs. Short-term flipping is dead in 2026.

4. You’re Targeting Student or Corporate Rentals

- Near universities (consistent demand)

- Corporate rentals (furnished, higher rents)

- Purpose-built, differentiated offering

5. You Can Tolerate Negative Cash Flow If you’re investing for long-term appreciation and have other income to cover shortfalls, negative cash flow is manageable. But ensure you can sustain it for 5-10 years.

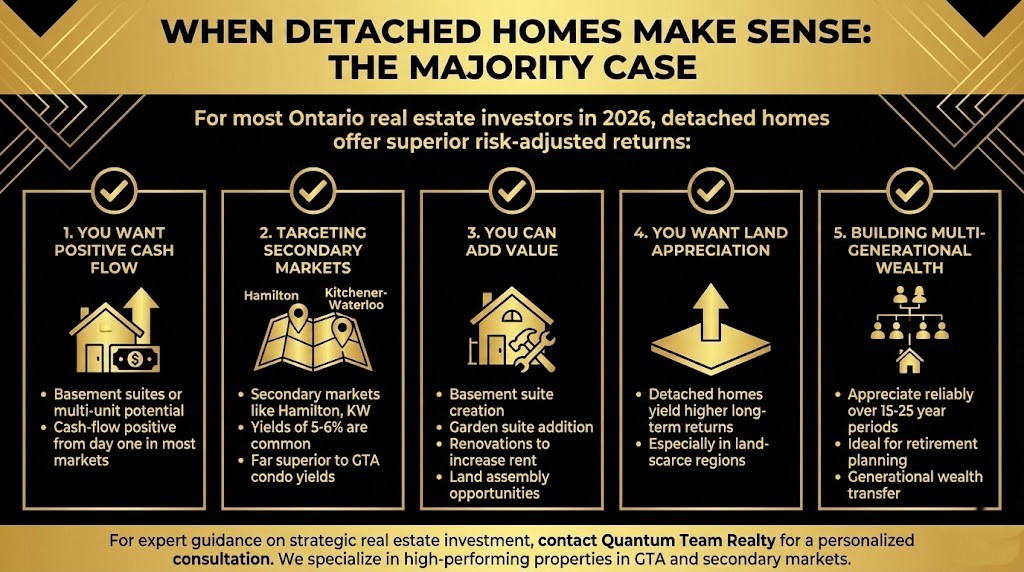

When Detached Homes Make Sense: The Majority Case

For most Ontario real estate investors in 2026, detached homes offer superior risk-adjusted returns:

✅ Detached Home Investing Works Best If:

1. You Want Positive Cash Flow With basement suites or multi-unit potential, detached homes cash-flow positive from day one in most markets.

2. You’re Targeting Secondary Markets In secondary markets such as Hamilton and Kitchener-Waterloo, yields of 5 to 6 percent are common—far superior to GTA condo yields.

3. You Can Add Value

- Basement suite creation

- Garden suite addition

- Renovations to increase rent

- Land assembly opportunities

4. You Want Land Appreciation In the long game, detached homes generally yield higher returns, especially in land-scarce regions.

5. You’re Building Multi-Generational Wealth Detached homes appreciate more reliably over 15-25 year periods, making them ideal for retirement planning or generational wealth transfer.

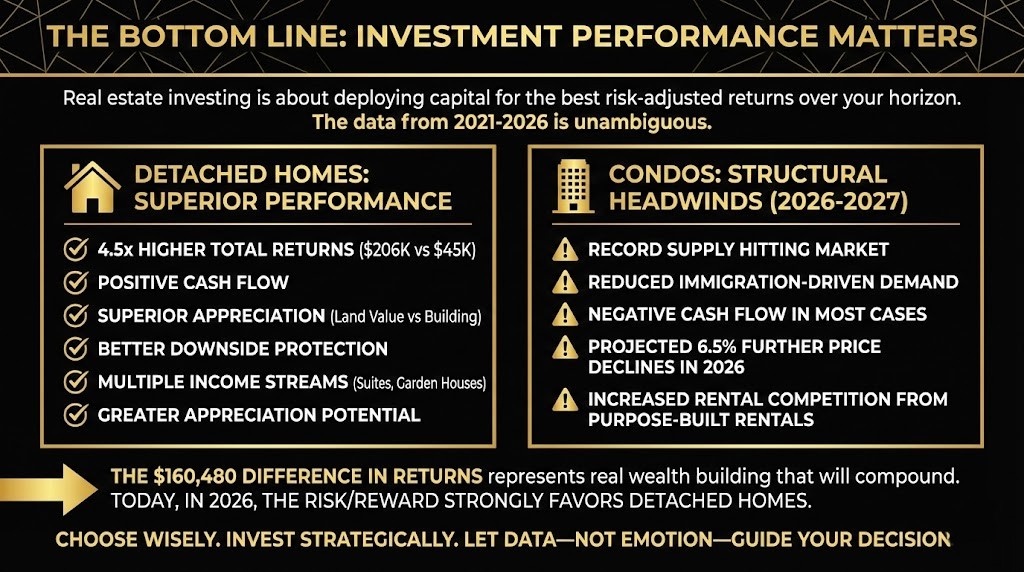

The Bottom Line: Investment Performance Matters

Real estate investing isn’t about choosing between property types based on personal preference—it’s about deploying capital where it generates the best risk-adjusted returns over your investment horizon.

The data from 2021-2026 is unambiguous:

Ontario detached homes outperformed condos by delivering:

- 4.5x higher total returns ($206K vs $45K in our scenarios)

- Positive cash flow versus negative cash flow

- Superior appreciation (land value vs building value)

- Better downside protection (smaller declines in corrections)

- Multiple income stream opportunities (suites, garden houses)

- Greater appreciation potential (land scarcity vs building supply)

Condos face structural headwinds through 2026-2027:

- Record supply hitting the market

- Reduced immigration-driven demand

- Negative cash flow in most cases

- Projected 6.5% further price declines in 2026

- Increased rental market competition from purpose-built rentals

This doesn’t mean condos are bad investments forever. Markets are cyclical. In 3-5 years, when current oversupply is absorbed and population growth rebounds, condos may offer attractive value. But today, in 2026, the risk/reward strongly favors detached homes for investors deploying capital in Ontario real estate.

The $160,480 difference in returns between our condo and detached scenarios isn’t theoretical—it represents real wealth building (or wealth destruction) that will compound over decades of investing.

Choose wisely. Invest strategically. Let data—not emotion or outdated assumptions—guide your decisions.

Partner With Quantum Team Realty for Strategic Investment Guidance

At Quantum Team Realty, we specialize in helping Ontario real estate investors make data-driven decisions that maximize returns while managing risk. Our team has successfully guided hundreds of clients through investment property acquisitions across the GTA, Niagara, Hamilton, and emerging secondary markets.

We provide comprehensive investment analysis including:

- Comparative return projections (5-year, 10-year, 15-year)

- Market-specific rental yield analysis

- Total cost of ownership calculations

- Cash flow modeling under various scenarios

- Market trend identification and timing strategies

- Property sourcing in high-performing neighborhoods

- Due diligence coordination (inspections, appraisals, legal)

Whether you’re evaluating your first investment property or building a portfolio of Ontario real estate, our experienced team delivers the local market knowledge and analytical rigor to help you invest confidently.

The difference between a mediocre investment and an exceptional one often comes down to market selection, timing, and strategy. Don’t leave $160,000+ in potential returns on the table by choosing the wrong property type or market.

Contact Quantum Team Realty today for a confidential investment consultation. We’ll analyze your capital, timeline, and objectives to identify the Ontario real estate investments positioned to deliver the strongest returns over your specific holding period.

Visit our comprehensive resources library for market reports, investment calculators, rental yield comparisons, and buyer guides—everything you need to make informed real estate investment decisions across Ontario.

Frequently Asked Questions

Should I invest in condos or detached homes in Ontario right now?

Based on 2025-2026 market conditions, detached homes offer superior risk-adjusted returns for most investors. Condos face ongoing price pressure from oversupply and are projected to decline another 6.5% in 2026, while detached homes are near stabilization (projected -1% in 2026). However, distressed condo purchases 15-20% below market in prime locations can work for patient investors with 10+ year horizons.

What's the typical rental yield for Ontario condos vs detached homes?

Toronto condos average 4.1% gross yield (2.1% net after expenses). Detached homes with basement suites in the GTA average 5.7% gross yield (3.8% net). In secondary markets like Hamilton and Kitchener-Waterloo, detached homes with suites can achieve 7%+ gross yields (5-6% net)—significantly outperforming condos.

Are condo prices going to keep falling in 2026?

Yes, most analysts project continued condo price declines of 5-7% in 2026 before stabilizing in 2027. The combination of record new supply, reduced immigration-driven demand, and investor exodus will keep downward pressure on prices. Stabilization depends on improved economic conditions and absorption of current oversupply.

Can I make money flipping condos in Ontario?

No. The condo flipping era ended in 2022. With prices declining, high transaction costs (land transfer tax, realtor commissions, legal fees totaling 5-7%), and sluggish turnover (38-45 days on market), short-term condo flipping is a losing strategy. Focus on long-term holds (7-10+ years) or avoid condos entirely.

What's the biggest risk with detached home investing?

The primary risks are: (1) higher initial capital requirement (need larger down payment), (2) tenant issues in multi-unit situations (basement suites require good screening), (3) major maintenance costs (roof, HVAC, foundation can be expensive), and (4) market-specific risks in declining suburbs. Mitigate by buying in growth markets, professional tenant screening, and maintaining capital reserves.

Should I sell my condo investment property?

If you purchased pre-2022 and have substantial equity, selling now might be wise to redeploy capital into higher-performing assets. If you’re underwater or close to purchase price, you may be better holding for 5-10 years for potential recovery. Run the numbers: if your annual negative cash flow exceeds projected appreciation, selling and reinvesting elsewhere (even taking a small loss) could make financial sense.

Are there any advantages to condo investing?

Yes: (1) lower entry cost (more accessible for first-time investors), (2) zero maintenance hassle (condo corp handles it), (3) amenities attract certain tenant demographics, (4) easier to manage remotely, and (5) strong rental demand in prime downtown locations. The question isn’t whether condos have advantages—it’s whether those advantages outweigh the current market headwinds and lower returns compared to detached homes.

Sunny Chadha

Sunny Chadha is the Co-Founder of Quantum Team Realty and brings over 15 years of experience in Niagara real estate. He is passionate about helping clients make informed decisions and sharing his deep knowledge of the local market.

References

- WOWA.ca. (January 7, 2026). “Toronto Housing Market Update.” Retrieved from wowa.ca/toronto-housing-market

- Toronto Regional Real Estate Board (TRREB). (Q3 2025). “Condo Market Report.” Retrieved from trreb.ca/market-data/condo-market-report

- blogTO. (December 9, 2025). “Average Toronto condo will lose almost $43,000 in value in 2026.” Retrieved from blogto.com

- nesto.ca. (January 2026). “Toronto Housing Market | 2026 Home Prices.” Retrieved from nesto.ca/toronto-housing-market-outlook

- Royal York Property Management. (2025). “Is 2025 the Right Year to Invest in a Rental Property in Ontario?” Retrieved from royalyorkpropertymanagement.ca

- bricksndreams.ca. (August 7, 2025). “Should You Invest in Condos or Detached Homes in Ontario?” Retrieved from bricksndreams.ca

- Milan Builders. (September 27, 2025). “Condo vs Detached Homes in Toronto: Which Offers Better Returns?” Retrieved from milanbuilders.ca

- RE/MAX Wealth Builders. (July 15, 2025). “Toronto Condo Investing in 2025: Is Now the Time to Get In?” Retrieved from remaxwealth.com

- Seventy Seven Park. (March 11, 2025). “Is the Toronto Condo Market Still a Good Investment in 2025?” Retrieved from seventysevenpark.com

- RE/MAX Canada. (April 22, 2025). “Are Condos a Good Investment?” Retrieved from blog.remax.ca

- TD Economics. (2026). “Provincial Housing Market Outlook.” Retrieved from economics.td.com/ca-provincial-housing-outlook

- precondo.ca. (August 22, 2025). “Toronto Real Estate Prices Housing Report (1967 to 2026).” Retrieved from precondo.ca/toronto-real-estate-prices

- Move Smartly. (January 2025). “Toronto Area Real Estate Market Report.” Retrieved from movesmartly.com/monthly-report-2025-january

- canadaimmigrants.com. (December 2025). “Toronto House Prices.” Retrieved from canadaimmigrants.com/average-house-price-in-toronto

- John Merrill, C21. (October 23, 2025). “Is Ontario real estate a smart investment right now?” Retrieved from john-merrill.c21.ca