When Rachel and David started saving for their first home in Toronto, they assumed they needed $150,000 for a 20% down payment on a $750,000 condo. They were shocked to discover they actually needed only $37,500 (5% down) and could access up to $19,975 in government rebates and tax savings to offset closing costs. By leveraging Ontario’s first-time home buyer incentives properly, they purchased their home three years sooner than planned and saved nearly $20,000 in upfront costs.

Yet thousands of Ontario first-time buyers miss these opportunities every year—simply because they don’t know they exist.

In 2026, Ontario offers one of North America’s most generous support systems for first-time home buyers, combining federal programs, provincial rebates, and municipal incentives. For Toronto buyers specifically, the total benefit can exceed $20,000 when all programs are stacked properly. Even outside Toronto, first-time buyers across Ontario can access $15,000+ in savings and tax advantages.

This comprehensive guide breaks down every first-time home buyer incentive available in Ontario for 2026, explaining eligibility requirements, maximum benefits, strategic stacking opportunities, and real-world scenarios showing exactly how much you can save.

Who Qualifies as a First-Time Home Buyer in Ontario?

Before diving into specific programs, understanding the “first-time buyer” definition is critical, as it varies slightly between programs

General Definition (Most Programs)

For most federal and provincial programs, you’re considered a first-time home buyer if:

✅ You have never owned or jointly owned a qualifying home anywhere in the world

✅ You did not live in a qualifying home owned by your spouse or common-law partner

✅ This applies to the current calendar year and the preceding four calendar years

This means if you owned a home 5+ years ago, you can qualify again as a “first-time buyer” for programs using this definition.

Ontario Land Transfer Tax Definition

Ontario’s land transfer tax rebate uses a lifetime definition: You must have never owned a home anywhere, at any time. Once you claim this rebate, you cannot qualify again—even if you sell and wait years before buying again.

The "Principal Residence" Requirement

Most programs require that the home be your principal place of residence within 9-12 months of purchase. Investment properties don’t qualify. However, you can rent out portions (basement suite) while living there.

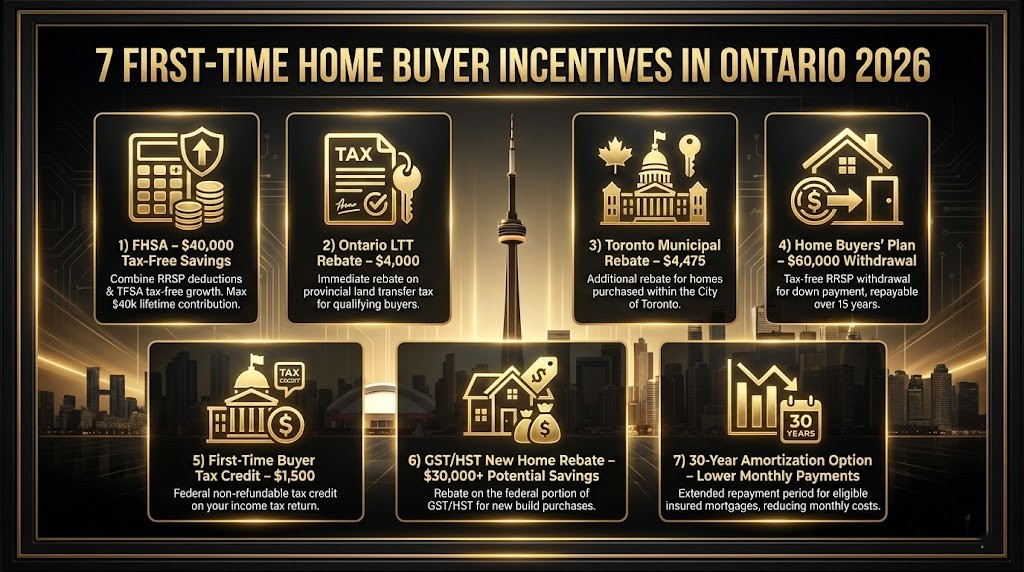

The 7 Major First-Time Home Buyer Incentives in Ontario (2026)

1. First Home Savings Account (FHSA): Tax-Free Growth + Deductions

Maximum Benefit: Up to $12,000 in tax savings + unlimited tax-free investment growth

The FHSA, launched in 2023, combines the best features of an RRSP and TFSA, making it the most powerful savings tool for Ontario first-time buyers.

How It Works:

| Feature | Details |

|---|---|

| Annual Contribution Limit | $8,000 per year |

| Lifetime Contribution Limit | $40,000 total |

| Tax Deduction | Contributions reduce taxable income (similar to RRSP) |

| Withdrawal Tax Treatment | Tax-free for qualifying home purchases (similar to TFSA) |

| Carryforward | Up to $8,000 unused room carries forward annually |

| Maximum Duration | 15 years from opening or until age 71 |

Sarah, an Ontario teacher earning $75,000 annually, opens an FHSA in 2026:

- Marginal tax rate: 29.65% (combined federal/provincial)

- Annual contribution: $8,000

- Immediate tax savings: $2,372 ($8,000 × 29.65%)

- Over 5 years: Contributes $40,000, saves $11,860 in taxes

- Investment growth (assume 5% annually): Earns $7,500 tax-free

- Total benefit: $19,360 ($11,860 tax savings + $7,500 growth)

Strategic Tips:

- Open your FHSA as soon as you’re eligible to start accumulating contribution room

- Couples can each open an FHSA, doubling the benefit to $80,000 combined savings

- Contributions are deductible in the year made OR can be carried forward if you expect higher income later

- Unlike RRSPs, you can’t deduct contributions made in the first 60 days of the following year

Critical Note: Any unused FHSA funds after 15 years or upon age 71 must be transferred to an RRSP/RRIF (taxable when withdrawn) or withdrawn and taxed as income.

For more strategies on maximizing your savings and avoiding costly mistakes, explore our comprehensive buyer resources and planning tools.

2. Ontario Land Transfer Tax Rebate: Up to $4,000

Maximum Benefit: $4,000 provincial rebate (covers LTT on homes up to $368,000)

Ontario charges land transfer tax on all property purchases. First-time buyers receive a rebate covering all or part of this tax.

Ontario Land Transfer Tax Rates:

| Purchase Price Bracket | Tax Rate |

|---|---|

| First $55,000 | 0.5% |

| $55,001 to $250,000 | 1.0% |

| $250,001 to $400,000 | 1.5% |

| $400,001 to $2,000,000 | 2.0% |

| Over $2,000,000 | 2.5% |

Examples:

| Home Price | LTT Payable | Rebate | You Pay |

|---|---|---|---|

| $300,000 | $2,975 | $2,975 | $0 |

| $368,000 | $4,950 | $4,000 | $950 |

| $500,000 | $6,475 | $4,000 | $2,475 |

| $750,000 | $12,950 | $4,000 | $8,950 |

Eligibility Requirements:

✅ Must be at least 18 years old

✅ Canadian citizen or permanent resident (as of closing or within 18 months)

✅ Never owned a home anywhere, at any time

✅ Must occupy home as principal residence within 9 months

✅ Can apply online, by mail, or at closing through your lawyer

Application Process: Your real estate lawyer typically claims this rebate at closing by completing the electronic land transfer tax affidavit. You receive the rebate immediately, reducing your closing costs.

3. Toronto Municipal Land Transfer Tax Rebate: Additional $4,475

Maximum Benefit: $4,475 municipal rebate (Toronto buyers only)

Toronto is the only major city in Ontario charging both provincial AND municipal land transfer tax. However, first-time buyers also receive a municipal rebate.

Toronto Municipal LTT Rates (Mirror Provincial):

The municipal rates match provincial rates, meaning Toronto buyers pay double the land transfer tax—but also receive double the rebate if they’re first-time buyers.

Combined Toronto Example:

| $500,000 Toronto Condo – Land Transfer Tax Breakdown | |

|---|---|

| Provincial LTT | $6,475 |

| Provincial Rebate | -$4,000 |

| Net Provincial | $2,475 |

| Municipal LTT | $6,475 |

| Municipal Rebate | -$4,475 |

| Net Municipal | $2,000 |

| Total LTT Owed | $4,475 |

| Total Savings | $8,475 |

Homes Under $400,000 in Toronto: First-time buyers pay $0 land transfer tax when purchasing homes under $400,000, as the combined rebates ($8,475) fully cover the combined LTT ($8,475).

For detailed breakdowns of closing costs across Ontario markets, see our Land Transfer Tax Calculator: Toronto vs. Niagara guide in our resources library.

4. Home Buyers' Plan (HBP): Access Your RRSP Tax-Free

Maximum Benefit: Withdraw up to $60,000 from RRSP ($120,000 for couples)

The HBP allows first-time buyers to withdraw RRSP funds for a down payment without paying withholding tax, provided you repay the amount over 15 years.

How It Works:

| Feature | Details |

|---|---|

| Maximum Withdrawal | $60,000 per person ($120,000 for couples) |

| Tax on Withdrawal | $0 (tax-free if repaid on schedule) |

| Repayment Period | 15 years (starting year 5 after withdrawal) |

| Annual Repayment | Minimum 1/15th of withdrawal amount |

| Missed Payments | Added to taxable income for that year |

Real-World Scenario:

David withdraws $60,000 from his RRSP in 2026 to buy his first home:

- 2026-2029: No repayment required (grace period)

- 2030: First repayment due: $4,000 (1/15 of $60,000)

- 2030-2044: Must repay $4,000 annually

- If David misses 2030 payment: $4,000 added to his taxable income, creating tax bill of $1,200-$1,600

FHSA vs HBP Comparison:

| Factor | FHSA | HBP |

|---|---|---|

| Tax on Contribution | Deductible | Deductible (when contributed to RRSP) |

| Tax on Withdrawal | Tax-free | Tax-free (if repaid) |

| Repayment Required? | No | Yes (15 years) |

| Reduces Retirement Savings? | No | Yes (until repaid) |

| Maximum Benefit | $40,000 | $60,000 |

Strategic Approach: Use FHSA first (no repayment), then supplement with HBP if needed for larger down payment.

5. First-Time Home Buyer Tax Credit (HBTC): $1,500 Federal Credit

Maximum Benefit: $1,500 federal tax credit (non-refundable)

This federal tax credit helps offset closing costs like legal fees, home inspections, and land transfer taxes.

How It Works:

- Claim up to $10,000 on your tax return

- Multiplied by lowest federal tax rate (15%)

- Result: $1,500 reduction in taxes owed

Example:

Michael purchased his first home in 2026 with $8,000 in closing costs:

- Claims $10,000 HBTC on 2026 tax return

- Reduces federal taxes owed by $1,500

- Either receives $1,500 refund OR pays $1,500 less tax

Eligibility: ✅ You or your spouse acquired a qualifying home ✅ Neither owned nor lived in a home you or spouse owned in current year or preceding 4 years ✅ Must intend to occupy as principal residence within one year

Strategic Tip: This is a non-refundable credit, meaning it only reduces taxes you owe. If you owe less than $1,500 in federal tax, you won’t receive the full benefit. Consider timing your home purchase in a year when you expect higher taxable income.

6. GST/HST New Housing Rebate: Up to $24,000 (New Construction)

Maximum Benefit: Up to $24,000 rebate on provincial HST portion for new homes

When purchasing a newly built home or substantially renovated property, buyers pay 13% HST in Ontario (5% GST + 8% provincial). The government rebates a portion of this tax.

Provincial HST Rebate (Ontario):

- Maximum rebate: $24,000 on the 8% provincial portion

- Applies to new homes purchased from builders

- Must be primary residence

Federal GST Rebate:

- Additional rebate on the 5% federal portion

- Varies by home price (maximum on homes under $350,000)

Example:

| $700,000 New Construction Home – HST Breakdown | |

|---|---|

| Total HST (13%) | $91,000 |

| Provincial Rebate (8% Portion) | -$24,000 |

| Federal Rebate (5% Portion) | ~$6,300 |

| Net HST Payable | $60,700 |

| Total Savings | $30,300 |

Eligibility: ✅ Purchasing newly built or substantially renovated home ✅ Will be primary residence ✅ Must apply within 2 years of closing

What Qualifies as “Substantially Renovated”? Generally means 90%+ of interior removed or replaced (excluding foundation, exterior walls, roof structure). Consult your lawyer to confirm eligibility.

To understand the total cost comparison between new builds and resale homes in Ontario, including this HST rebate benefit, read our detailed analysis in the buyer resources section.

7. 30-Year Amortization for First-Time Buyers (New 2024)

Maximum Benefit: Reduced monthly payments of $150-$300

Starting in late 2024, first-time home buyers purchasing newly built homes with insured mortgages (less than 20% down) can now access 30-year amortizations—previously only available with 20%+ down.

Impact on Monthly Payments:

$600,000 Mortgage at 4.5% Interest:

| Amortization | Monthly Payment | Total Interest (Full Term) |

|---|---|---|

| 25 Years | $3,330 | $399,000 |

| 30 Years | $3,040 | $494,400 |

| Monthly Savings (30 vs 25) | $290 | – |

| Additional Interest Cost (30-Year) | – | +$95,400 |

When This Makes Sense: ✅ You need lower monthly payments to qualify for mortgage ✅ Cash flow is tight in early years (expect income growth later) ✅ Buying in high-priced markets where affordability is stretched

When to Avoid: ❌ You can afford 25-year payments comfortably ❌ Minimizing total interest cost is priority ❌ Planning to make lump-sum prepayments

Strategic Approach: Start with 30-year amortization for affordability, then make extra payments to reduce amortization over time. Most mortgages allow 15-20% annual prepayments without penalty.

Stacking Incentives: Maximum Savings Scenario

This represents the real financial advantage of properly leveraging all available first-time buyer programs in Ontario’s highest-cost market.

Municipal Homeownership Programs (Select Ontario Cities)

Beyond provincial and federal programs, several Ontario municipalities offer additional down payment assistance:

Oakville

- Down payment loans (forgivable or interest-free)

- Check town website for current programs

Burlington

- First-time buyer assistance programs

- Income and price restrictions apply

Mississauga

- Periodic down payment assistance initiatives

- Monitor city website for announcements

Hamilton

- Down payment loans for eligible buyers

- Targeted to specific income brackets

Important: Municipal programs have limited funding and strict eligibility criteria. Apply early and maintain contact with housing departments for program availability.

Common Mistakes First-Time Buyers Make

❌ Mistake #1: Not Opening FHSA Early Enough

Many buyers wait until they’re “ready to buy” before opening an FHSA. This wastes potential contribution room.

Solution: Open your FHSA as soon as you’re eligible (age 18+, first-time buyer status), even if purchasing is 5+ years away. Contribution room accumulates, and earlier opening maximizes tax-free growth.

❌ Mistake #2: Assuming 20% Down is Required

As detailed in our 5 Real Estate Myths That Cost Ontario Buyers Thousands guide, the belief that 20% down is mandatory prevents many buyers from entering the market years sooner.

Reality: Minimum down payment is 5% (up to $500,000) or 5% + 10% on the portion above $500,000 (for homes $500K-$1.5M). With CMHC insurance, you can buy sooner and leverage appreciation while building equity.

❌ Mistake #3: Forgetting to Apply for Rebates

Some buyers discover Ontario’s land transfer tax rebate months after closing—losing thousands because they missed the 18-month application window.

Solution: Work with an experienced real estate lawyer who automatically processes all rebates at closing. Your lawyer should claim both provincial and Toronto municipal rebates (if applicable) on your behalf.

❌ Mistake #4: Not Combining FHSA + HBP

Buyers often think it’s “either FHSA or HBP.” Both can be used for the same home purchase.

Example:

- FHSA contribution: $40,000

- HBP withdrawal: $60,000

- Total: $100,000 down payment (single buyer)

- Couples: $200,000 combined ($80K FHSA + $120K HBP)

❌ Mistake #5: Missing the New Construction HST Rebate

New home buyers often pay full 13% HST without realizing they qualify for up to $24,000 in provincial rebates.

Solution: Confirm your builder includes HST rebate applications in closing documents. If buying resale that was “substantially renovated,” consult your lawyer about rebate eligibility.

Step-by-Step Action Plan for Ontario First-Time Buyers

12+ Months Before Buying:

- ✅ Open FHSA immediately (start accumulating contribution room)

- ✅ Contribute $8,000 annually to FHSA

- ✅ Build RRSP for potential HBP use

- ✅ Check credit score and improve if needed (target 680+ for best rates)

- ✅ Research neighborhoods and realistic pricing

6-12 Months Before Buying:

- ✅ Get mortgage pre-approval to confirm buying power

- ✅ Calculate total down payment available (FHSA + HBP + savings)

- ✅ Research municipal programs for additional assistance

- ✅ Factor closing costs: 1.5-4% of purchase price (legal, inspection, etc.)

- ✅ Connect with experienced buyer’s agent

0-6 Months (Active Buying):

- ✅ Begin home search with clear budget and priorities

- ✅ Make offers with conditions (inspection, financing)

- ✅ Finalize mortgage (consider 30-year amortization if needed)

- ✅ Hire real estate lawyer who handles LTT rebates automatically

- ✅ Claim First-Time Buyer Tax Credit on next year’s tax return

For personalized guidance through every step of this process, contact Quantum Team Realty for a confidential consultation with our experienced first-time buyer specialists.

The Bottom Line: $20,000+ in Savings Await

Ontario’s first-time home buyer incentives represent one of North America’s most comprehensive support systems for new homeowners. Between federal programs (FHSA, HBP, HBTC), provincial rebates (LTT), municipal rebates (Toronto MLTT), and new home rebates (GST/HST), first-time buyers can access:

- $15,000-$20,000 in direct rebates and credits

- $11,000-$12,000 in tax savings (FHSA contributions over 5 years)

- $3,000-$5,000 in reduced monthly payments (30-year amortization first year)

- Tax-free investment growth on FHSA savings

The difference between buyers who leverage these programs and those who don’t can easily exceed $25,000 in first-year benefits alone—money that reduces closing costs, strengthens down payments, and improves long-term affordability.

But these benefits only help if you know they exist and use them strategically.

The most successful first-time buyers don’t just know about these programs—they maximize them through proper timing, stacking multiple incentives, and working with professionals who ensure nothing is missed.

Partner With Quantum Team Realty

At Quantum Team Realty, we specialize in guiding Ontario first-time home buyers through the complete incentive landscape. Our team has helped hundreds of first-time buyers access every available dollar of government support, saving them tens of thousands in closing costs and improving their long-term financial outcomes.

We provide:

- Complete incentive eligibility assessment for your situation

- Strategic planning to maximize FHSA, HBP, and rebate benefits

- Connections to mortgage brokers who structure optimal financing

- Real estate lawyer referrals who never miss rebate applications

- Neighborhood guidance matching your budget and priorities

- Post-purchase support for tax credit claims and financial planning

The difference between maximizing available incentives and leaving money on the table often comes down to expertise. Our first-time buyer specialists know exactly which questions to ask, which programs stack together, and how to time your purchase for maximum benefit.

Don’t leave $20,000+ in government support unclaimed.

Contact Quantum Team Realty today for a complimentary first-time buyer consultation. We’ll assess your eligibility for all available programs, calculate your potential savings, and create a strategic action plan for your successful home purchase.

Access our complete library of first-time buyer resources, calculators, and planning guides to start your journey toward homeownership with confidence and clarity.

Frequently Asked Questions

Can I use first-time buyer incentives if I owned property years ago?

For most federal programs (FHSA, HBP, HBTC), you qualify again if you haven’t owned or lived in a home owned by you or your spouse in the current year and preceding 4 calendar years. However, Ontario’s land transfer tax rebate uses a lifetime definition—if you’ve ever owned property anywhere, you don’t qualify, even if it was decades ago.

My spouse owned a home before we met. Do I still qualify?

For Ontario LTT rebate, yes—it’s based on your individual ownership history, not your spouse’s. For federal programs (FHSA, HBP), you don’t qualify if you lived in a home owned by your spouse during the 4-year lookback period after you became spouses.

Can I withdraw from my FHSA to buy an investment property?

No. FHSA withdrawals are tax-free only if used to purchase a qualifying home you’ll occupy as your principal residence within one year. Investment property purchases trigger taxation on the withdrawal.

What happens if I don't buy a home after opening an FHSA?

You have 15 years to use FHSA funds or until you turn 71, whichever comes first. If unused, you must either: (1) Transfer tax-free to RRSP/RRIF (taxable when withdrawn from RRSP/RRIF later), or (2) Withdraw and pay income tax immediately. There’s no penalty beyond normal taxation.

Do I need to repay my FHSA withdrawal like the Home Buyers' Plan?

No. This is the FHSA’s biggest advantage over HBP. FHSA withdrawals are permanently tax-free with no repayment requirement. HBP withdrawals must be repaid to your RRSP over 15 years or the amount is added to taxable income.

Can I buy a home with my partner if only one of us is a first-time buyer?

Yes, but rebates are reduced. For Ontario LTT rebate, the first-time buyer can claim 50% of the maximum rebate ($2,000 instead of $4,000) based on their ownership share. For FHSA, each person’s account is individual—the first-time buyer can use their $40,000 FHSA contribution for the joint purchase.

How do I apply for the Ontario land transfer tax rebate?

Your real estate lawyer typically handles this at closing by completing the electronic land transfer tax affidavit. You can also apply online through Ontario’s Ministry of Finance portal within 18 months of closing. Most buyers let their lawyer process it automatically to avoid missing deadlines.

Sunny Chadha

Sunny Chadha is the Co-Founder of Quantum Team Realty and brings over 15 years of experience in Niagara real estate. He is passionate about helping clients make informed decisions and sharing his deep knowledge of the local market.

References

- Government of Ontario. (2022). “Land Transfer Tax Refunds for First-Time Homebuyers.” Retrieved from ontario.ca/document/land-transfer-tax

- WOWA.ca. (2026). “Ontario First-Time Home Buyer Incentives for 2026.” Retrieved from wowa.ca/calculators/ontario-first-time-home-buyer-incentives

- ThinkInsure. (2025). “First Time Home Buyer Incentives | 2025 Update.” Retrieved from thinkinsure.ca/insurance-help-centre

- The Martin Group. (2025). “Government Incentives for First-Time Home Buyers Ontario 2025.” Retrieved from themartingroup.ca/blog

- nesto.ca. (September 2025). “First-Time Home Buyers Incentives in Ontario.” Retrieved from nesto.ca/mortgage-basics

- Sunlite Mortgage. (January 2026). “First-Time Home Buyer incentives in Ontario.” Retrieved from sunlitemortgage.ca/ontario

- The Mortgage Advisors. (August 2025). “What Is the Ontario Land Transfer Tax Rebate?” Retrieved from themortgageadvisors.ca

- Ratehub.ca. (January 2026). “First-Time Home Buyer Programs in Canada in 2026.” Retrieved from ratehub.ca/first-time-home-buyer-programs

- Government of Canada. (2026). “First Home Savings Account (FHSA).” Retrieved from canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account

- Government of Canada. (2026). “Participating in your FHSAs.” Retrieved from canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account/contributing-your-fhsa

- TD Canada Trust. (2026). “First Home Savings Account (FHSA).” Retrieved from td.com/ca/en/personal-banking/personal-investing/products/registered-plans/fhsa

- RBC Wealth Management. (December 2025). “FHSA: 9 Questions Answered About the New First Home Savings Account.” Retrieved from ca.rbcwealthmanagement.com

- CIBC. (2026). “First Home Savings Account (FHSA).” Retrieved from cibc.com/en/personal-banking/investments/fhsa

- Sun Life Canada. (2026). “FHSA contribution limits.” Retrieved from sunlife.ca/en/investments/fhsa/contributions

- Desjardins. (2026). “Open an FHSA in Canada.” Retrieved from desjardins.com/en/savings-investment/savings-plans/fhsa