When Wei, a Chinese national working in Shanghai, purchased a $900,000 condo in Toronto in January 2025, she was shocked to discover her closing costs included an additional $225,000 in Non-Resident Speculation Tax (NRST)—plus another $90,000 in Toronto’s new Municipal NRST. Combined, these foreign buyer taxes added $315,000 (35% of the purchase price) to her transaction costs, on top of regular land transfer taxes.

However, Wei’s immigration lawyer informed her that if she obtains permanent residency within four years and occupies the condo as her principal residence, she can reclaim the entire $315,000 through rebate applications.

This scenario illustrates both the substantial financial impact of Ontario’s Non-Resident Speculation Tax and the opportunities for relief available to eligible foreign nationals. For international buyers, new immigrants, students, and foreign workers purchasing Ontario real estate in 2026, understanding the NRST is critical—the difference between knowing the rules and missing opportunities can easily cost hundreds of thousands of dollars.

This comprehensive guide explains everything foreign buyers need to know about Ontario’s NRST in 2026, including who pays, current rates, available exemptions, rebate eligibility, Toronto’s additional municipal tax, and strategic planning considerations.

What is the Non-Resident Speculation Tax?

The Non-Resident Speculation Tax (NRST) is an additional land transfer tax charged by Ontario when foreign nationals purchase residential property in the province. Introduced in April 2017 at 15% for the Greater Golden Horseshoe region, the NRST has evolved significantly:

Evolution of NRST:

| Date | Rate | Geographic Scope | Impact |

|---|---|---|---|

| April 21, 2017 | 15% | Greater Golden Horseshoe only | Initial implementation |

| March 30, 2022 | 20% | Province-wide | Expanded coverage |

| October 25, 2022 | 25% | Province-wide | Current rate |

| January 1, 2025 | 25% + 10% | Toronto adds Municipal NRST | 35% combined in Toronto |

Sources: Government of Ontario, City of Toronto, 2025-2026

The NRST applies in addition to Ontario’s regular land transfer tax. This means foreign buyers pay both the standard LTT (approximately 1.5-2.5% depending on purchase price) and the 25% NRST surcharge.

Toronto's Additional Municipal NRST (2025)

Effective January 1, 2025, Toronto introduced a 10% Municipal Non-Resident Speculation Tax (MNRST) on top of the provincial NRST. This makes Toronto the most expensive city in Canada for foreign real estate investment.

Toronto Foreign Buyer Tax Breakdown (2026):

$1,000,000 Toronto Home Purchase by Foreign National:

- Provincial Land Transfer Tax: ~$16,475

- Toronto Municipal Land Transfer Tax: ~$16,475

- Provincial NRST (25%): $250,000

- Toronto MNRST (10%): $100,000

- Total Closing Taxes: $382,950 (38.3% of purchase price)

For detailed breakdowns of land transfer taxes across Ontario, including rebates available to first-time buyers, explore our comprehensive resources and calculators covering all closing cost scenarios.

What Activity Looks Like

- 60-hour work weeks

- Constant availability

- Reactive client management

- Individual problem-solving

- Marketing created from scratch each time

- Isolated decision-making

- No backup when deals get complex

What Growth Looks Like

- Strategic client acquisition systems

- Team support handling logistics

- Proactive market positioning

- Collective intelligence informing strategy

- Shared marketing infrastructure

- Collaborative negotiation approach

- Backup expertise on complex transactions

Who Must Pay NRST?

The NRST applies to three categories of buyers:

1. Foreign Nationals

A “foreign national” is any individual who is not a Canadian citizen or permanent resident of Canada, as defined under the Immigration and Refugee Protection Act.

Examples of Foreign Nationals:

- International students studying in Canada on study permits

- Foreign workers on temporary work permits

- Visitors on tourist visas

- Individuals on any non-permanent immigration status

2. Foreign Corporations

Any corporation that is not incorporated in Canada or is controlled by foreign nationals qualifies as a foreign entity subject to NRST.

“Control” is determined by:

- Ownership of voting shares (50%+ by foreign nationals)

- De facto control by foreign entities

- Indirect control through parent companies

3. Taxable Trustees

Trustees holding property for the benefit of foreign nationals or foreign corporations must pay NRST unless they qualify for specific trust exemptions (mutual fund trusts, REITs, SIFT trusts).

What Properties Are Subject to NRST?

Covered Properties:

✅ Detached houses

✅ Semi-detached houses

✅ Townhouses

✅ Condominium units (residential)

✅ Properties containing 1-6 single-family residences

✅ NEW (March 27, 2024): Standalone condo parking spaces and storage lockers

NOT Covered:

❌ Properties with 7+ residential units (apartment buildings)

❌ Purely commercial properties

❌ Agricultural land (unless containing residential structures)

❌ Industrial properties

March 2024 Amendment: Parking & Storage Units

Prior to March 27, 2024, foreign buyers could purchase standalone condo parking spaces or storage lockers without paying NRST because these weren’t classified as “residential land.” This loophole has been closed.

Now: If a foreign national buys a parking spot or storage locker in a condo complex (without simultaneously purchasing a residential unit), the standalone accessory unit is subject to 25% NRST.

Transitional Relief: Agreements of purchase and sale signed before March 27, 2024, are exempt from this rule even if closing occurs after that date.

NRST Exemptions: Who Doesn't Pay?

Several categories of foreign nationals can purchase Ontario property without paying NRST if they meet specific criteria:

Exemption 1: Ontario Immigrant Nominee Program (OINP)

Foreign nationals nominated under the OINP who have applied for permanent residency before their nominee certificate expires are exempt from NRST.

Requirements:

- Valid OINP certificate

- Permanent residency application submitted before certificate expiry

- Property will be principal residence

- ll joint purchasers must also qualify (citizens, PRs, or nominees)

Exemption 2: Protected Persons (Refugees)

Individuals granted protected person status under Canada’s Immigration and Refugee Protection Act are exempt from NRST.

Requirements:

- Valid protected person status documentation

- Property will be principal residence

- All joint purchasers must also qualify

Exemption 3: Spouse of Canadian or PR

Foreign nationals purchasing property jointly with a spouse who is a Canadian citizen or permanent resident are exempt from NRST.

Critical Requirements:

- Both spouses must be named as purchasers on title

- Property will be principal residence for both

- Must be legally married or common-law spouses at time of closing

- "Spouse" definition: married OR cohabiting continuously for 3+ years OR parents of a child together

Trap to Avoid: Becoming spouses after closing doesn’t qualify. You must be spouses on the closing date.

Claiming Exemptions

Exemptions must be claimed at the time of property registration through Ontario’s electronic land registration system (Teraview). Your real estate lawyer completes the required affidavits certifying your eligibility.

No exemption is automatic. Failure to properly claim an exemption at closing means paying the full NRST, though you may apply for a refund later if eligibility is proven.

NRST Rebates: Getting Your Money Back

Even if you pay NRST at closing, you may be eligible for a full rebate under certain circumstances.

Primary Rebate: Permanent Resident Status

The most common and valuable rebate is available to foreign nationals who become permanent residents of Canada within four years of purchasing their property.

Permanent Resident NRST Rebate Requirements:

| Requirement | Details |

|---|---|

| Become PR within 4 years | Permanent residency must be approved within four years from the purchase/closing date. |

| Paid NRST | The Non-Resident Speculation Tax must have been paid at closing (not claimed as an exemption). |

| Principal Residence | The property must be occupied as the principal residence throughout the eligibility period. |

| Occupancy Timing | The buyer must move into the property within 60 days of closing. |

| Continuous Occupancy | The property must remain the primary residence continuously until the rebate is approved. |

| Spouse Requirement | If purchased with a spouse, only one spouse needs to become a permanent resident within the 4-year period. |

| Sole / Spousal Ownership | The property must be owned only by the foreign national (and their spouse, if applicable). |

Rebate Amount: If eligible, 100% of NRST paid is refunded (including Toronto’s 10% MNRST).

Real-World Example:

Marco, an Italian national, purchased a $750,000 Toronto condo in March 2025:

- Provincial NRST paid: $187,500 (25%)

- Toronto MNRST paid: $75,000 (10%)

- Total foreign buyer tax: $262,500

Marco received permanent residency approval in January 2028 (2 years 10 months later). He occupied the condo as his principal residence from May 2025 through his rebate application in February 2028.

Result: Marco received a $262,500 rebate—100% of both taxes refunded.

Industrial Use Rebate (New: November 2025)

A new NRST rebate became available for conveyances on or after November 6, 2025, for residential properties repurposed for industrial use.

Requirements: ✅ Property was originally residential ✅ Converted to industrial use after purchase ✅ Proper zoning and permits obtained ✅ Foreign entity still owns property

This targets scenarios where foreign entities purchase residential land for legitimate business/industrial development rather than speculation.

Phased-Out Rebates (No Longer Available)

Important Update: As of March 31, 2025, transitional rebates for international students and foreign workers are no longer available.

Previously, foreign nationals who became full-time students at Ontario universities or began working in Ontario under valid work permits could apply for NRST rebates. These transitional provisions expired, and applications filed after March 31, 2025, are no longer accepted.

For current information on all available programs for foreign nationals and new immigrants, visit our comprehensive buyer resources center with up-to-date guides and eligibility tools.

How to Apply for NRST Rebates

Ontario offers an online application portal through the Ministry of Finance for NRST rebate and refund applications.

Step 1: Gather Required Documentation

- Proof of NRST payment (statement of adjustments, land transfer tax statement)

- Permanent resident card or confirmation of permanent residence

- Proof of occupancy (utility bills, driver’s license, lease agreements if applicable)

- Purchase agreement and closing documents

- Government-issued photo ID

Step 2: Submit Online Application

- Access Ontario Ministry of Finance NRST online portal

- No login or password required

- Complete electronic affidavit

- Upload supporting documents

- Provide banking information for refund deposit

Step 3: Ministry Review

- Processing time: typically 4-8 weeks

- Ministry may request additional documentation

- Verification of occupancy and PR status

Step 4: Rebate Issued

- Direct deposit to provided banking information

- Full amount of NRST + MNRST (if applicable)

Application Deadline: You must apply within 4 years from the date NRST became payable (closing date). Missing this deadline means forfeiting your rebate—even if you otherwise qualify.

Section 20 Relief: Discretionary Tax Relief

Beyond standard exemptions and rebates, Ontario’s Land Transfer Tax Act Section 20 grants the Minister of Finance discretion to provide relief where “special circumstances” make it “inequitable” for the taxpayer to pay the full tax.

When Section 20 Relief May Apply:

- Unique hardship situations

- Extraordinary circumstances beyond taxpayer control

- Technical compliance issues that resulted in improper NRST assessment

- Cases where strict application of rules produces unfair outcomes

Important Notes: ❌ Relief is not automatic—each case is individually evaluated ❌ Persuading the Ministry to exercise discretion is challenging ❌ Strong legal representation often necessary ❌ Must demonstrate why ordinary exemptions/rebates don’t address your situation

Recent Case: In Yavari v. Ontario, a foreign national who became a PR applied for NRST rebate but faced denial due to technical compliance issues. The case illustrates how strictly the Ministry interprets occupancy and principal residence requirements.

If you believe you qualify for Section 20 relief, consulting with a tax lawyer specializing in NRST is strongly recommended. Contact Quantum Team Realty for referrals to experienced NRST legal specialists who can assess your situation.

The Federal Foreign Buyer Ban: Additional Restrictions

In addition to provincial NRST, foreign nationals face a federal prohibition on purchasing Canadian residential property.

Federal Ban Timeline:

| Period | Status |

|---|---|

| January 1, 2023 – January 1, 2025 | Initial 2-year ban |

| February 4, 2024 | Extension announced |

| January 1, 2025 – January 1, 2027 | Extended ban period |

Who is Prohibited: ❌ Foreign nationals (non-citizens, non-PRs) ❌ Foreign corporations ❌ Anyone not a Canadian citizen or permanent resident

Exceptions to Federal Ban: ✅ Temporary residents (students, workers) meeting specific criteria ✅ Refugees ✅ Properties in certain rural areas ✅ Commercial/recreational properties (not residential)

The federal ban works alongside NRST—even if you’re willing to pay 25-35% in speculation taxes, you may still be legally prohibited from purchasing depending on your immigration status and property type.

Real-World Cost Scenarios

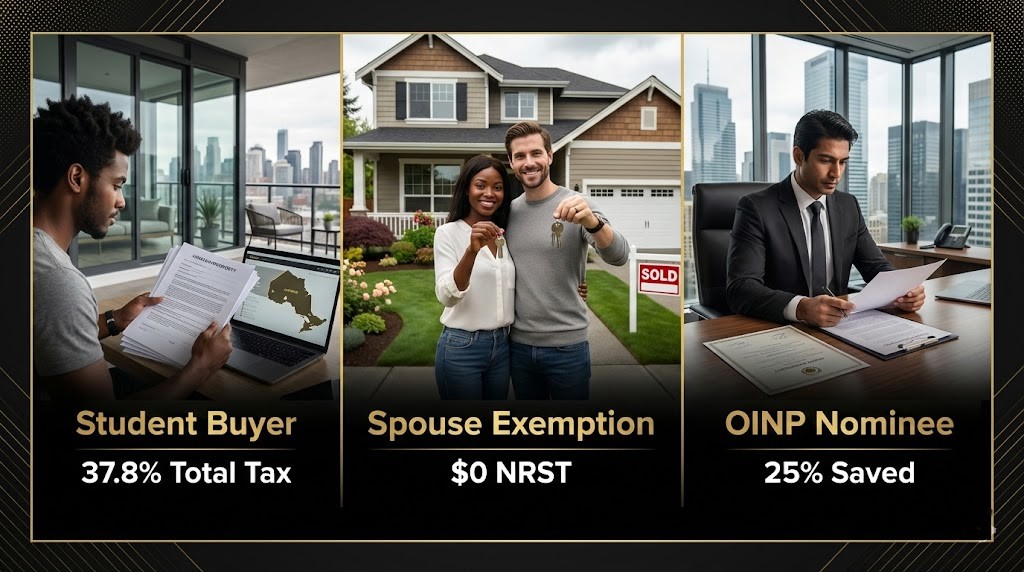

Scenario 1: International Student (Toronto)

Background: Priya, studying at University of Toronto on a study permit, purchases a $600,000 condo near campus in March 2026.

Costs:

- Provincial Land Transfer Tax: $8,475

- Toronto Municipal LTT: $8,475

- Provincial NRST (25%): $150,000

- Toronto MNRST (10%): $60,000

- Total Taxes: $226,950 (37.8% of purchase)

Path to Rebate:

- Priya applies for permanent residency through Canadian Experience Class in 2027

- Receives PR approval in December 2028 (2 years 9 months after purchase)

- Occupies condo as principal residence from April 2026 through December 2028

- Applies for rebate in January 2029

- Receives $210,000 refund (NRST + MNRST only; regular LTT not refundable)

Note: International student and foreign worker rebates were eliminated March 31, 2025. Priya’s only path to rebate is achieving PR status.

Scenario 2: Foreign Worker Married to Canadian (Mississauga)

Background: Juan, a Mexican citizen on a work permit, purchases a $850,000 home with his Canadian spouse Maria in 2026.

Costs:

- Provincial Land Transfer Tax: $12,950

- Provincial NRST: $0 (exempt – married to Canadian)

Why No NRST: Juan qualifies for the spouse exemption because:

✅ Both Juan and Maria are listed as purchasers

✅ Maria is a Canadian citizen

✅ Property will be their shared principal residence

✅ They were legally married at closing

Total Tax Savings: $212,500 (25% NRST exemption)

Scenario 3: OINP Nominee (Ottawa)

Background: Chen, nominated through Ontario Immigrant Nominee Program, purchases a $550,000 townhouse in Ottawa before his nominee certificate expires.

Costs:

- Provincial Land Transfer Tax: $7,725

- Provincial NRST: $0 (exempt – OINP nominee)

Why No NRST: Chen qualifies for OINP exemption because:

✅ Valid OINP certificate

✅ Permanent residency application submitted before certificate expiry

✅ Property will be principal residence

✅ Exemption properly claimed at closing

Total Tax Savings: $137,500 (25% NRST exemption)

For comprehensive closing cost calculations and eligibility assessments specific to your situation, explore our buyer planning resources and tools.

Common Mistakes and How to Avoid Them

❌ Mistake #1: Not Claiming Exemptions at Closing

Many eligible foreign nationals pay NRST unnecessarily because they don’t realize exemptions exist or their lawyer doesn’t properly claim them during registration.

Solution: Inform your lawyer of your immigration status (OINP nominee, spouse of Canadian, etc.) well before closing so proper affidavits are prepared.

❌ Mistake #2: Missing the 4-Year Rebate Window

Foreign nationals who become PRs often forget to apply for NRST rebates within the 4-year deadline.

Solution: Set calendar reminders starting 3 years after purchase to begin gathering documentation. Don’t wait until year 4.

❌ Mistake #3: Purchasing Before Marriage is Formalized

A foreign national and their Canadian partner buy a property together while common-law, expecting the spouse exemption. If they don’t meet the technical definition of “spouse” at closing (3+ years cohabitation or parents of a child), NRST applies.

Solution: Delay purchase until you’ve cohabited continuously for 3+ years, or formalize marriage before closing.

❌ Mistake #4: Inadequate Occupancy Documentation

Applying for rebate 3 years later without proof of continuous occupancy as principal residence results in denial.

Solution: Build a “rebate file” starting at closing: utility bills, bank statements, driver’s license, tax returns, employer letters—anything showing the address as your primary residence.

❌ Mistake #5: Buying in Toronto Without Accounting for 10% MNRST

Foreign buyers budgeting for 25% NRST discover they need an additional 10% for Toronto’s municipal tax—$100,000+ on a $1 million purchase.

Solution: Always verify whether your property is within City of Toronto boundaries (not just “Greater Toronto Area”). MNRST only applies within Toronto’s city limits.

The Bottom Line: NRST is Substantial But Refundable

Ontario’s Non-Resident Speculation Tax represents one of the highest foreign buyer taxes globally:

- 25% provincial NRST across all of Ontario

- Additional 10% municipal MNRST in Toronto (35% combined)

- Applies to virtually all residential property transactions

- Significantly impacts purchase affordability

However, the tax isn’t necessarily permanent:

- 100% rebate available if you become a PR within 4 years

- Exemptions available for OINP nominees, refugees, and spouses

- Strategic planning can legally minimize or eliminate the tax

The difference between foreign buyers who successfully navigate NRST and those who lose hundreds of thousands comes down to:

- Understanding eligibility for exemptions before purchase

- Documenting occupancy from day one for potential rebates

- Applying within deadlines (4 years, no extensions)

- Working with experienced professionals who specialize in NRST

For foreign nationals, new immigrants, and international families considering Ontario real estate, NRST isn’t a reason to avoid purchasing—it’s a reason to plan carefully and work with experts who can guide you through exemptions, rebates, and strategic timing.

Partner With Quantum Team Realty

At Quantum Team Realty, we regularly work with foreign nationals, new immigrants, international students, and foreign workers navigating Ontario’s complex real estate landscape. Our team understands the nuances of NRST, exemption eligibility, rebate applications, and strategic purchase timing.

We provide:

- NRST impact assessment based on your specific immigration status

- Exemption eligibility review and strategy development

- Referrals to real estate lawyers specializing in NRST compliance

- Connections to immigration lawyers for PR pathway planning

- Purchase timing guidance to maximize savings

- Documentation strategy for principal residence requirements

- Post-purchase support for rebate applications

The difference between paying $200,000+ in NRST permanently versus receiving a full rebate often comes down to proper planning and expert guidance.

Don’t navigate NRST alone—the stakes are too high.

Contact Quantum Team Realty today for a confidential consultation about your Ontario real estate purchase. We’ll assess your NRST exposure, identify available exemptions or rebate opportunities, and create a strategic plan that protects your investment.

Frequently Asked Questions

Can I get an NRST refund if I become a Canadian citizen instead of just a permanent resident?

Yes. Becoming a Canadian citizen makes you eligible for the permanent resident rebate, as citizens are treated the same as PRs for NRST purposes. The key is achieving PR or citizenship status within 4 years of purchase.

Does the NRST apply if I buy a property through a Canadian corporation I own?

Potentially yes. If you’re a foreign national and own 50%+ of the corporation’s voting shares, the corporation is considered a “foreign entity” subject to NRST. However, complex ownership structures may create exemptions—consult a tax lawyer.

What happens if I sell my property before getting permanent residency?

You lose eligibility for the NRST rebate. The rebate requires continuous occupancy as principal residence from closing until rebate approval. Selling before receiving PR means you paid NRST with no path to recovery.

Can I rent out my property while waiting for my rebate application to be processed?

No. You must occupy the property as your principal residence continuously from closing through rebate application. Renting it out—even partially—disqualifies you.

I'm a Canadian citizen living abroad. Do I have to pay NRST if I buy property in Ontario?

No. NRST is based on citizenship/PR status, not residency. Canadian citizens are exempt regardless of where they live.

Does the 4-year deadline to become a PR start from closing date or purchase agreement date?

The 4-year period runs from the closing date (when NRST became payable), not the agreement signing date. This is also the deadline for filing your rebate application.

Can my spouse claim the rebate if I become a PR but my spouse remains a foreign national?

Yes. If you purchased jointly and either spouse becomes a PR within 4 years, the full rebate is available—as long as both continued occupying the property as principal residence.

Sunny Chadha

Sunny Chadha is the Co-Founder of Quantum Team Realty and brings over 15 years of experience in Niagara real estate. He is passionate about helping clients make informed decisions and sharing his deep knowledge of the local market.

References

- Government of Ontario. (2025). “Non-Resident Speculation Tax.” Retrieved from ontario.ca/document/non-resident-speculation-tax

- Government of Ontario. (November 2025). “Non-Resident Speculation Tax Collected.” Retrieved from ontario.ca/document/non-resident-speculation-tax/non-resident-speculation-tax-collected

- Government of Ontario. (November 2025). “Non-Resident Speculation Tax Rebates and Refunds.” Retrieved from ontario.ca/document/non-resident-speculation-tax/non-resident-speculation-tax-rebates-and-refunds

- Taxpayer Law. (September 2025). “Ontario NRST in 2025: The Complete, Current Guide.” Retrieved from taxpayer.law/ontario-nrst-in-2025

- Green and Spiegel LLP. (August 2024). “What You Need to Know About Foreign Buyer’s Tax in Canada.” Retrieved from gands.com/blog/2024/03/06/what-you-need-to-know-about-foreign-buyers-tax-in-canada

- Tax Law Canada. (August 2025). “Exemptions and rebates (Section 20) of the NRST.” Retrieved from taxlawcanada.com/exemptions-and-rebates-section-20-of-the-non-resident-speculation-tax-nrst

- Taxpayer Law. (October 2025). “Ontario NRST and Toronto MNRST FAQ.” Retrieved from taxpayer.law/nrst-faq

- City of Toronto. (March 2024). “Municipal Non-Resident Speculation Tax (MNRST).” Retrieved from toronto.ca/home/311-toronto-at-your-service

- Government of Canada. (February 2024). “Extension of the Prohibition on the Purchase of Residential Property by Non-Canadians Act.” Retrieved from canada.ca

- GovtSchemes.org. (November 2025). “Non-Resident Speculation Tax Section 20 Exemptions & Rebates 2025.” Retrieved from govtschemes.org